Bitcoin carnage resumes with another 10% skid

Crypto guru Barry Silbert used the weekend selloff to build up his portfolio

Crypto guru Barry Silbert used the weekend selloff to build up his portfolio

Market-timing system’s previous buy sign occurred at the January 2018 lows

Russian, Saudi oil ministers may gather at G-20 meeting: analyst

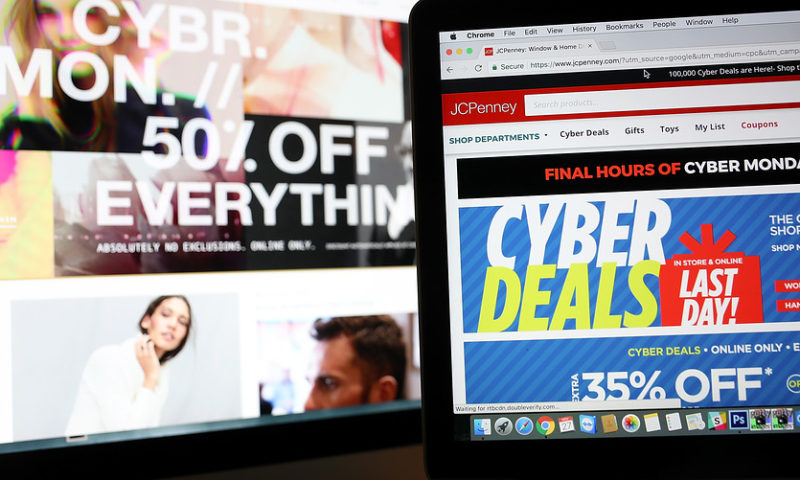

The online shopping holiday is expected to generate $7.8 billion in sales this year

Why Diptyque, Net-a-Porter and other companies are peddling their product lines with fancy holiday Advent calendars

London markets found support Monday after a Brexit deal was approved over the weekend between the U.K. and the European Union, and a rebound in crude oil prices lifted some big-name energy stocks.

US fund investors renewed their concerns about credit quality in corporate debt markets during the latest week, hitting leveraged loan and high-yield debt funds with multibillion-dollar withdrawals, Lipper data showed on Friday.

New York: US stocks closed lower Friday, bumping the benchmark S&P 500 index into a correction, or drop of 10 per cent or more from its recent all-time high in September. Energy companies led the market slide as the price of U.S. crude oilNSE 1.23 % tumbled to its lowest level in more than a year, reflecting worries among traders that a slowing global economy could hurt demand for oil.

Mr Market was largely directionless and indecisive during the week gone by, as it whipsawed its way awaiting triggers from local and global markets.

Solar stocks have taken it on the chin in 2018, but that could present a buying opportunity for shares of SolarEdge Technologies, First Solar, and TerraForm Power.

US Government confirms Social Security payment on May 7 only for these retirees and disability beneficiaries

US Government confirms Social Security payment on May 7 only for these retirees and disability beneficiaries Americans are more worried about running out of money in retirement than dying. Experts offer ways to reduce that risk

Americans are more worried about running out of money in retirement than dying. Experts offer ways to reduce that risk Spirit Airlines gets approval for NYSE American listing

Spirit Airlines gets approval for NYSE American listing Archer Aviation (NYSE:ACHR) Partners With United Airlines For New York City Air Taxi Network

Archer Aviation (NYSE:ACHR) Partners With United Airlines For New York City Air Taxi Network Trump embraces ‘tailored’ tariff deals as foreign leaders look to sweeten their offers

Trump embraces ‘tailored’ tariff deals as foreign leaders look to sweeten their offers Why some are accusing Trump of manipulating stock markets

Why some are accusing Trump of manipulating stock markets Bezos-backed Slate Auto unveils affordable EV truck

Bezos-backed Slate Auto unveils affordable EV truck Big brands are officially worried about American shoppers

Big brands are officially worried about American shoppers Intel CFO says tariffs increase chance for economic slowdown, recession getting likelier

Intel CFO says tariffs increase chance for economic slowdown, recession getting likelier Fed’s Kashkari nervous that trade policy uncertainty will lead to layoffs

Fed’s Kashkari nervous that trade policy uncertainty will lead to layoffs