OpenAI files for IPO, the latest in a stream of possible AI mega-sales

OpenAI has confidentially filed for an initial public offering, setting it up for what may…

The Signal Institutional Traders Track Most Reveals Market-Moving Opportunities

The Signal Institutional Traders Track Most Reveals Market-Moving Opportunities Q4 Earnings Outperformers: Graham Corporation (NYSE:GHM) And The Rest Of The Engineered Components and Systems Stocks

Q4 Earnings Outperformers: Graham Corporation (NYSE:GHM) And The Rest Of The Engineered Components and Systems Stocks Assessing Best Buy (NYSE:BBY) Valuation After Q1 Beat And Guidance Reaffirmation

Assessing Best Buy (NYSE:BBY) Valuation After Q1 Beat And Guidance Reaffirmation Americans grow more pessimistic about finances as rent and food cost fears surge, Fed says

Americans grow more pessimistic about finances as rent and food cost fears surge, Fed says From unfilled gas tanks to fewer frills, consumers rethink spending

From unfilled gas tanks to fewer frills, consumers rethink spending Russia Slashes Oil Exports As Fuel Shortages And Drone Attacks Bite

Russia Slashes Oil Exports As Fuel Shortages And Drone Attacks Bite OpenAI files for IPO, the latest in a stream of possible AI mega-sales

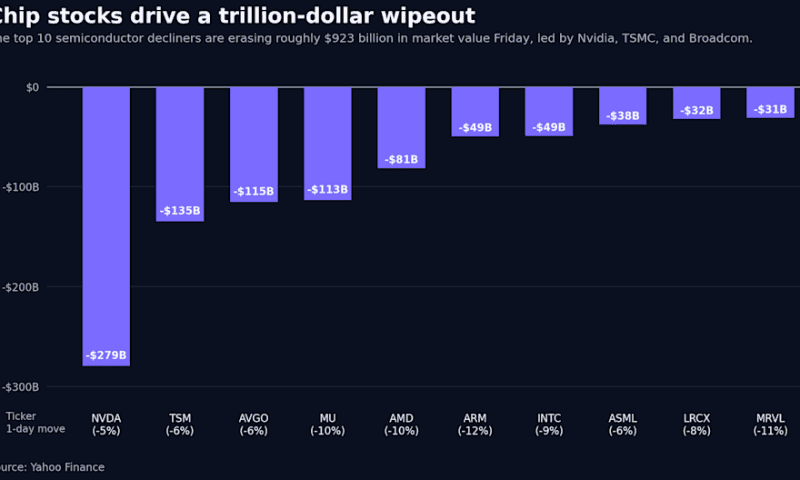

OpenAI files for IPO, the latest in a stream of possible AI mega-sales Asia chip-linked shares recover after U.S. peers bounce back

Asia chip-linked shares recover after U.S. peers bounce back Lilly shares rise on hopes that next-gen drug will extend lead in weight-loss market

Lilly shares rise on hopes that next-gen drug will extend lead in weight-loss market A Look At Antero Midstream (NYSE:AM) Valuation After Recent Share Price Consolidation

A Look At Antero Midstream (NYSE:AM) Valuation After Recent Share Price Consolidation