Industrial equipment and engineered products manufacturer Albany (NYSE:AIN) missed Wall Street’s revenue expectations in Q4 CY2024, with sales falling 11.3% year on year to $286.9 million. The company’s full-year revenue guidance of $1.22 billion at the midpoint came in 6% below analysts’ estimates. Its non-GAAP profit of $0.58 per share was 12% below analysts’ consensus estimates.

Is now the time to buy Albany? Find out in our full research report.

Albany (AIN) Q4 CY2024 Highlights:

Revenue: $286.9 million vs analyst estimates of $299.5 million (11.3% year-on-year decline, 4.2% miss)

Adjusted EPS: $0.58 vs analyst expectations of $0.66 (12% miss)

Adjusted EBITDA: $218.9 million vs analyst estimates of $59.65 million (76.3% margin, significant beat)

Management’s revenue guidance for the upcoming financial year 2025 is $1.22 billion at the midpoint, missing analyst estimates by 6% and implying -1.3% growth (vs 8.1% in FY2024)

EBITDA guidance for the upcoming financial year 2025 is $250 million at the midpoint, below analyst estimates of $276.8 million

Operating Margin: 8.5%, down from 12.9% in the same quarter last year

Free Cash Flow Margin: 21%, up from 12.2% in the same quarter last year

Market Capitalization: $2.50 billion

“We continue to perform well in both our businesses, as evidenced by strong results at Machine Clothing and ongoing operational progress steered by new leadership at Engineered Composites,” said Gunnar Kleveland, President and Chief Executive Officer.

Company Overview

Founded in 1895, Albany (NYSE:AIN) is a global textiles and materials processing company, specializing in machine clothing for paper mills and engineered composite structures for aerospace and other industries.

General Industrial Machinery

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand for general industrial machinery companies. Those who innovate and create digitized solutions can spur sales and speed up replacement cycles, but all general industrial machinery companies are still at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Albany’s 3.1% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the industrials sector and is a rough starting point for our analysis.

Albany Quarterly Revenue

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Albany’s annualized revenue growth of 9% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

Albany Year-On-Year Revenue Growth

We can better understand the company’s revenue dynamics by analyzing its most important segments, Machine Clothing and Engineered Composites, which are 65.6% and 34.4% of revenue. Over the last two years, Albany’s Machine Clothing revenue (paper manufacturing belts) averaged 11.4% year-on-year growth while its Engineered Composites revenue (aerospace components) averaged 7.3% growth.

This quarter, Albany missed Wall Street’s estimates and reported a rather uninspiring 11.3% year-on-year revenue decline, generating $286.9 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Albany has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 15.7%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Albany’s operating margin decreased by 7.8 percentage points over the last five years. This raises an eyebrow about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

Albany Trailing 12-Month Operating Margin (GAAP)

This quarter, Albany generated an operating profit margin of 8.5%, down 4.4 percentage points year on year. Since Albany’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Albany, its EPS declined by 5% annually over the last five years while its revenue grew by 3.1%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Albany Trailing 12-Month EPS (Non-GAAP)

Diving into the nuances of Albany’s earnings can give us a better understanding of its performance. As we mentioned earlier, Albany’s operating margin declined by 7.8 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Albany, its two-year annual EPS declines of 9.5% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Albany reported EPS at $0.58, down from $1.22 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Albany’s full-year EPS of $3.17 to grow 21.3%.

Key Takeaways from Albany’s Q4 Results

We were impressed by how significantly Albany blew past analysts’ EBITDA expectations this quarter. On the other hand, its full-year revenue guidance missed significantly and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2.1% to $77.20 immediately following the results.

Albany underperformed this quarter, but does that create an opportunity to invest right now? We think that the latest quarter is just one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

Theater company AMC Entertainment (NYSE:AMC) announced better-than-expected revenue in Q4 CY2024, with sales up 18.3% year on year to $1.31 billion. Its non-GAAP loss of $0.18 per share was 10.2% below analysts’ consensus estimates.

Is now the time to buy AMC Entertainment? Find out in our full research report.

AMC Entertainment (AMC) Q4 CY2024 Highlights:

Revenue: $1.31 billion vs analyst estimates of $1.29 billion (18.3% year-on-year growth, 1.6% beat)

Adjusted EPS: -$0.18 vs analyst expectations of -$0.16 (10.2% miss)

Adjusted EBITDA: $164.8 million vs analyst estimates of $128.8 million (12.6% margin, 27.9% beat)

Operating Margin: 0.4%, up from -13.6% in the same quarter last year

Free Cash Flow was $113.9 million, up from -$149.9 million in the same quarter last year

Market Capitalization: $1.45 billion

Company Overview

With a profile that was raised due to meme stock mania beginning in 2021, AMC Entertainment (NYSE:AMC) operates movie theaters primarily in the US and Europe.

Leisure Facilities

Leisure facilities companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted their spending from “things” to “experiences”. Leisure facilities seek to benefit but must innovate to do so because of the industry’s high competition and capital intensity.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Over the last five years, AMC Entertainment’s demand was weak and its revenue declined by 3.3% per year. This was below our standards and is a sign of lacking business quality.

AMC Entertainment Quarterly Revenue

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. AMC Entertainment’s annualized revenue growth of 8.9% over the last two years is above its five-year trend, but we were still disappointed by the results. Note that COVID hurt AMC Entertainment’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

AMC Entertainment Year-On-Year Revenue Growth

This quarter, AMC Entertainment reported year-on-year revenue growth of 18.3%, and its $1.31 billion of revenue exceeded Wall Street’s estimates by 1.6%.

Looking ahead, sell-side analysts expect revenue to grow 10.8% over the next 12 months. While this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Cash Is King

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While AMC Entertainment posted positive free cash flow this quarter, the broader story hasn’t been so clean. Over the last two years, AMC Entertainment’s demanding reinvestments to stay relevant have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 7.8%, meaning it lit $7.80 of cash on fire for every $100 in revenue.

AMC Entertainment Trailing 12-Month Free Cash Flow Margin

AMC Entertainment’s free cash flow clocked in at $113.9 million in Q4, equivalent to a 8.7% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

Over the next year, analysts predict AMC Entertainment will continue burning cash, albeit to a lesser extent. Their consensus estimates imply its free cash flow margin of negative 6.4% for the last 12 months will increase to negative 2.5%.

Key Takeaways from AMC Entertainment’s Q4 Results

We were impressed by how significantly AMC Entertainment blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its EPS missed significantly. Zooming out, we think this was a decent quarter featuring some areas of strength but also some blemishes. The stock traded up 4.6% to $3.43 immediately following the results.

Is AMC Entertainment an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

Nvidia (NVDA) reported its fourth quarter earnings after the bell on Wednesday, beating analysts’ expectations on the top and bottom lines and issuing solid Q1 guidance.

Nvidia’s stock was up as much as 2% on the news; near 6:00 p.m. ET, the stock was up closer to 0.7%.

Nvidia’s earnings come as the company girds itself for potential 25% tariffs on chips imported into the US and the threat of increased export controls on its shipments to China. The AI giant is also contending with the fallout from claims that Chinese startup DeepSeek developed its AI models using less powerful Nvidia chips than its US rivals, putting into question whether Big Tech companies are over-investing in AI.

For the quarter, Nvidia reported earnings per share (EPS) of $0.89 on revenue of $39.3 billion. Wall Street was expecting EPS of $0.84 on revenue of $38.2 billion. The company said it expects Q1 revenue of $43 billion plus or minus 2%, better than the $42.3 billion expected.

Data center revenue clocked in at $35.6 billion versus expectations of $34 billion in the quarter.

“We’ve successfully ramped up the massive-scale production of Blackwell AI supercomputers, achieving billions of dollars in sales in its first quarter,” CEO Jensen Huang said in a statement. “AI is advancing at light speed as agentic AI and physical AI set the stage for the next wave of AI to revolutionize the largest industries.”

According to Nvidia CFO Colette Kress, cloud service providers made up 50% of Nvidia’s data center revenue in the quarter. The company reported similar results in Q3.

The company’s Blackwell line of chips contributed billions in sales for the quarter, Kress said.

“We delivered $11.0 billion of Blackwell architecture revenue in the fourth quarter of fiscal 2025, the fastest product ramp in our company’s history.”

Nvidia’s gaming revenue, however, fell 11% year over year in Q4 due to supply constraints around its latest gaming chips.

Nvidia is the reigning champion of AI chips, and it’s not losing that crown anytime soon. Its chips are the envy of Silicon Valley and beyond, and its competitors are still far from overtaking its performance advantage.

Big Tech companies Amazon (AMZN), Google (GOOG, GOOGL), Meta (META), and Microsoft (MSFT) are spending billions of dollars building out their AI data centers, and a chunk of that is going straight to Nvidia.

But shares of those same companies are also struggling in the early months of 2025.

Google parent Alphabet is off more than 8% year to date, Amazon is down 2.5%, Microsoft has fallen 5.3%, and Apple (AAPL) has dropped more than 4%.

Meta is the sole outlier in the group, with shares up over 14%.

Huang also alluded to fears that DeepSeek’s AI models, which were developed using lower-powered Nvidia chips while still matching the performance of top US-made AI models, would hurt Nvidia’s sales.

“Demand for Blackwell is amazing as reasoning AI adds another scaling law — increasing compute for training makes models smarter and increasing compute for long thinking makes the answer smarter,” he said.

Nvidia is staring down President Trump’s threat of 25% tariffs on chips imported into the US, which could force it to either raise prices or eat some of the cost of the tariffs, cutting into margins. Nvidia works with TSMC to build its processors, which produces many of those chips in Taiwan.

Trump has also threatened to put further export restrictions on Nvidia chips destined for China, which would cut into the company’s revenue from the region.

Wall Street has also raised concerns about the impact of Amazon, Google, Microsoft, and Meta using their own custom AI chips versus those developed by Nvidia. If those companies’ chips can match Nvidia’s in performance, the thinking goes, they’ll be less dependent on Nvidia’s offerings.

But Morgan Stanley Research analyst Joseph Moore cautioned overreacting to the potential of these ASICS, or application-specific integrated circuits.

“Spending time with 20-25 Nvidia alternatives over the years, most of which failed to get traction, we saw initial enthusiasm based on price and potential performance, which [brought] an initial deployment,” Moore wrote. “Then there is almost always a pull back to Nvidia, which has the most mature ecosystem, and the alternatives are put on hold, sometimes never to return.”

Google’s and Amazon’s chips have proven to be the exception to that rule so far, but Moore says Nvidia is still gaining share in the AI space.

Washington Post owner Jeff Bezos on Wednesday announced a “significant shift” to the publisher’s opinion page that led David Shipley, the paper’s editorial page editor, to leave the paper. The changes upended precedent and rattled a media company that has already been shaken by years of turmoil and leadership turnover.

As part of the overhaul, the Post will publish daily opinion stories on two editorial “pillars”: personal liberties and free markets, Bezos teased in an X post on Wednesday morning after announcing the change in a company-wide email. The Post’s opinion section will cover other subjects, too, Bezos wrote, but “viewpoints opposing those pillars will be left to be published by others.”

“I’m confident that free markets and personal liberties are right for America,” Bezos wrote. “I also believe these viewpoints are underserved in the current market of ideas and news opinion. I’m excited for us together to fill that void.”

In announcing the shift, the billionaire media mogul championed the changes as based in American principles anchored in “freedom.” This freedom, Bezos emphasized, “is ethical — it minimizes coercion — and practical — it drives creativity, invention, and prosperity.”

As a basis for the change, Bezos noted that legacy opinion sections have become outdated and have been replaced by the internet.

“There was a time when a newspaper, especially one that was a local monopoly, might have seen it as a service to bring to the reader’s doorstep every morning a broad-based opinion section that sought to cover all views,” Bezos said via X. “Today, the internet does that job.”

David Shipley leaves the Post

Bezos also shared that David Shipley, the Post’s editorial page editor, would part ways with the company. Shipley had been offered a role in leading Bezos’ planned changes but decided to step away instead.

“I offered David Shipley, whom I greatly admire, the opportunity to lead this new chapter,” Bezos wrote on X. “I suggested to him that if the answer wasn’t ‘hell yes,’ then it had to be ‘no.’ After careful consideration, David decided to step away. This is a significant shift, it won’t be easy, and it will require 100% commitment — I respect his decision.”

Bezos said the Post will search for a new opinion editor to “own” the paper’s new editorial direction.

In an email to the Post’s editorial team obtained by CNN, Shipley noted his decision to leave the publisher was reached “after reflection on how I can best move forward in the profession I love.”

“I will always be thankful for the opportunity I was given to work alongside a team of opinion journalists whose commitment to strong, innovative, reported commentary inspired me every day — and was affirmed by two Pulitzer Prizes and two Loeb Awards in two short years,” Shipley wrote in the email.

Shipley’s departure comes after spending four months navigating increasing criticism of the Post from subscribers and its own journalists. During that time, he defended the Post’s decision to not run a cartoon from Ann Telnaes that featured Jeff Bezos – and led to her resignation.

“Not every editorial judgment is a reflection of a malign force,” Shipley said in January. “My decision was guided by the fact that we had just published a column on the same topic as the cartoon and had already scheduled another column — this one a satire — for publication. The only bias was against repetition.”

Post staffers lash out

Bezos’ announcement was immediately met with hostility by some Post staffers who publicly took issue with the move.

Jeff Stein, the publisher’s chief economics reporter, called the overhaul a “massive encroachment by Jeff Bezos” that makes it clear “dissenting views will not be published or tolerated there.”

“I still have not felt encroachment on my journalism on the news side of coverage, but if Bezos tries interfering with the news side I will be quitting immediately and letting you know,” Stein said on X.

Amanda Katz, who stepped down from her role on the Post’s opinion team at the end of 2024, called the change “an absolute abandonment of the principles of accountability of the powerful, justice, democracy, human rights, and accurate information that previously animated the section in favor of a white male billionaire’s self-interested agenda.” And columnist Philip Bump, who pens the Post’s weekly “How to Read This Chart” newsletter, pithily said “what the actual f**k” on Bluesky.

Meanwhile, conservatives are celebrating Bezos’ changes. Charlie Kirk, the Turning Point USA founder, hailed the change as “the culture (…)changing rapidly for the better.” And Elon Musk, whose SpaceX is a direct rival of Bezos’ Blue Origins, succinctly applauded on X, saying “Bravo, @JeffBezos!”

Following the transformation’s internal announcement, Will Lewis, the paper’s publisher and chief executive, noted in an internal email obtained by CNN that the “recalibrate(ion)” was “not about siding with any political party,” but, rather, about “being crystal clear about what we stand for as a newspaper.”

“Doing this is a critical part of serving as a premier news publication across America and for all Americans,” Lewis wrote to Post staffers.

As Shipley exits the Post on Friday, Lewis said he would put together an interim arrangement, adding that the editorial page editor’s replacement would be announced in “due course” — and be “someone who is wholehearted in their support for free markets and personal liberties.”

In the early afternoon, Matt Murray, the Post’s executive editor, chimed in to respond to the “questions” he had received from concerned staffers. In an email obtained by CNN, Murray toed Bezos’ line, reminding staffers that opinion sections are “traditionally the provenance of the owner at news organizations.”

“The independent and unbiased work of The Post’s newsroom remains unchanged, and we will continue to pursue engaging, impactful journalism without fear or favor,” Murray wrote.

Though Murray and Lewis have supported Bezos’ transformation with staffers, New York magazine reports that Lewis’ tune is quite different behind the scenes, having warned Bezos that the changes would likely negatively impact the publication.

Already, Lewis’ private predictions appear to be manifesting. Since the announcement, two former top Post editors have come out against the move. As reported by the Daily Beast, Marty Baron, the Post’s former executive editor, said he was “sad and disgusted” by Bezos’ demands, emphasizing that the Amazon and Blue Origin founder “has prioritized those commercial interests over The Post, and he is betraying The Post’s longstanding principles to do so.”

Meanwhile, Cameron Barr, a former senior managing editor for the Post, said in a LinkedIn post that he would end his “professional association” with the newspaper, saying Bezos’ changes represent “an unacceptable erosion of its commitment to publishing a healthy diversity of opinion and argument.” And David Maraniss, a longtime Post editor and Pulitzer Prize winner, said on Bluesky that he would “never write for (the Post) again as long as (Bezos is) the owner.”

Bezos and the Post’s new direction

The divisive overhaul comes months after Bezos blocked the opinion page’s endorsement of former Vice President Kamala Harris at the eleventh hour, ending decades of precedent. Shipley was among the chorus of voices that sought to convince Bezos not to bar the endorsement, telling staffers in October that “I failed” to do just that.

Since Bezos’ action to block the op-ed, a chain reaction has hounded the Post, with 250,000 Post readers canceling their subscriptions and several opinion staffers resigning in protest. The Post has also hemorrhaged reporters, who have signed with rival publications rather than remain at the ailing outlet.

The massive changeup comes months after Bezos admitted in his defense of the op-ed block that his Amazon and Blue Origin business interests have served as a “complexifier for the Post.”

In the run-up to November’s election, Silicon Valley media moguls were seen cozying up to then-candidate Donald Trump, hedging their bets in the event of a conservative presidential victory. Critics said Bezos was trying to change the Post’s editorial strategy to gain favorability with Trump, who has grown close to Elon Musk, whose SpaceX is a direct rival of Bezos’ own business. Bezos pushed back on those accusations in a rare October op-ed.

“When it comes to the appearance of conflict, I am not an ideal owner of The Post,” Bezos wrote. “You can see my wealth and business interests as a bulwark against intimidation, or you can see them as a web of conflicting interests.”

“Only my own principles can tip the balance from one to the other,” he wrote in October.

Bezos’ “appearance of conflict” is issued from his numerous holdings, which include his Amazon and spacefaring company, Blue Origin. Bezos’ Amazon is also still facing a lawsuit from the FTC and 17 states, who accuse the company of abusing its economic dominance and harming fair competition.

Bezos attended President Trump’s January inauguration. Although Bezos was not the only tech billionaire present, his attendance as the Post’s owner did little to dispel the appearance of conflict.

Most recently, the Post opted to not publish an anti-Musk wrap ad for its print edition; while the Post did greenlight an internal anti-Musk ad, it has not yet clarified the grounds on which the wrap was denied and did not comment when asked whether Bezos was involved with the decision.

Post staffers also have for some time also been discontented with Bezos over his appointment of Lewis as publisher and chief executive. After taking the top job in early 2024, reports quickly emerged of Lewis’ involvement in several controversies, including accusations that he used fraudulent and unethical methods to acquire reporting for articles while working at the Sunday Times. Lewis also came under fire for allegedly attempting to kill a story about his alleged involvement in the phone hacking scandal coverup. Lewis has denied the accusations.

Dissatisfaction with Lewis reached a peak in June, when two Pulitzer Prize-winning Post journalists called for a leadership change amid the reports that questioned Lewis’ journalistic integrity, undermining the Post’s reputation and reporting alike.

Though, as Murray notes, the opinion section is the “provenance” of the Post’s owner — meaning Bezos — the billionaire’s last change resulted in the loss of hundreds of thousands of subscribers, worsening the Post’s financial woes. As the overhaul exacerbates longstanding issues at the storied publication and current and former Post staffers publicly decry the changes, the Post appears to find itself in an emergency.

The American consumer is getting worried about the economy.

Economic jitters are showing up across various sentiment surveys as the Trump administration aims to reconfigure America’s trade relationship with the world and inflation shows signs of getting stuck.

The latest evidence comes from The Conference Board’s Consumer Confidence Index for February, released Tuesday morning. The index fell to 98.3, falling for the third-straight month and marking the largest monthly decline since August 2021, as expectations for inflation in the year ahead climbed. That coincides with the trends reflected in the University of Michigan’s consumer survey for February.

Homebuilders are also growing worried, according to the National Association of Home Builders; even US small businesses, which remain somewhat optimistic about deregulation and tax cuts, are in doubt about the economy’s future. The National Federation of Independent Business’ Uncertainty Index rose in January to its third-highest reading on record.

America’s souring economic mood, driven by worries over President Donald Trump’s aggressive approach to tariffs, is a stunning reversal from the (brief) burst of optimism after President Donald Trump’s election in November.

“The fact that consumers don’t feel like it’s smooth sailing — you’ve got one very obvious suspect. That’s the White House, which is sowing uncertainty just about everywhere, whether it comes to trade policy or foreign policy,” Justin Wolfers, economics professor at the University of Michigan, told CNN’s Pamela Brown. “I genuinely understand why consumers are nervous and I hope this doesn’t turn out to be a self-inflicted own goal.”

The Fed and inflation fears

For the Federal Reserve, it’s critical that Americans have faith that inflation will eventually return to normal in the long run. Central bankers pay close attention to people’s perception of prices because they can be self-fulfilling: If Americans expect inflation to pick up, they modify their spending accordingly.

So far, Fed officials in recent speeches haven’t sounded the alarm on inflation expectations. But some have expressed the importance that expectations remain in check.

If Trump’s policies cause inflation to pick up, “it could be appropriate to ignore or look through an increase in the price level if the impact on inflation is expected to be brief and limited,” St. Louis Fed President Alberto Musalem said at a recent event in New York. “However, a different monetary policy response could be appropriate if higher inflation is sustained, or long-term inflation expectations rise.”

“I would be especially concerned by evidence suggesting (inflation expectations) are becoming unanchored,” Musalem said.

Chicago Fed President Austan Goolsbee said Sunday in an interview with News Nation that the run-up in inflation expectations reflected in the University of Michigan’s survey “wasn’t a great number.”

“But it’s only one month of data. You need at least two or three months for that to count,” he said.

For example, when consumer sentiment fell to a record low in June 2022, as inflation reached a four-decade high, Americans continued to spend.

But today’s economic landscape is rife with uncertainty, which may be affecting people’s spending plans, according to a new Wells Fargo survey released Tuesday. About three-quarters of 3,657 adults and 203 teens surveyed across the country said they plan to reduce their spending, citing uncertainty in the economy.

“Consumer behaviors are shifting,” said Michael Liersch, head of advice and planning at Wells Fargo, in a release. “The value of the dollar and what it is providing may not be as predictable anymore, which seems to be more pronounced for younger Americans.”

The survey showed that 82% of Gen Z adults and 79% of Millennials plan to pare back their spending in the coming months. Eating out or food delivery gave respondents the most sticker shock, according to the survey, followed by a tank of gas and prices for concerts or sporting events.

Richmond Fed president Tom Barkin said Tuesday that he wants to keep interest rates “modestly restrictive” until he gains more confidence inflation is returning to the central bank’s 2% goal, warning about lessons learned from the 1970s.

“It makes sense to stay modestly restrictive until we are more confident inflation is returning to our 2% target,” Barkin said in a speech in Richmond, Va.

“It is critical that we remain steadfast,” he added. “We learned in the ’70s that if you back off inflation too soon, you can allow it to reemerge. No one wants to pay that price.”

The Fed kept its rates on hold at its meeting last month following three consecutive cuts as central bankers grew more cautious about the future path of inflation and the potential effects of new trade, tax, and immigration policies from the Trump administration.

The central bank is expected to keep rates on hold at a meeting next month. But traders are now betting the Fed is likely to resume cutting in June and could do so again in September as they digest a survey that showed consumer confidence fell this month while inflation expectations surged.

The challenge for the Fed, Barkin said Tuesday, is there is a lot of uncertainty now with how policy changes from Washington will impact the economy, as well as with geopolitical conflicts and natural disasters.

Barkin noted that he had seen economic analyses of tariffs levied in 2018 under President Donald Trump’s first administration, and they concluded those duties increased inflation by about 30 basis points.

But he said the policies this time won’t be exactly the same, and policymakers don’t know whether recent experience with inflation will exacerbate or mitigate the impact this time. Barkin questioned whether firms will be more willing to pass costs on or if consumers will resist further price increases.

He also pointed to uncertainty around deregulation, taxes, and spending, as well as immigration changes, and what impact all of that could have on the workforce.

“I prefer to wait and see how this uncertainty plays out and how the economy responds,” he said.

Barkin is the latest Fed official to offer some words of caution about the Fed’s stance. St. Louis Fed president Alberto Musalem last Thursday also aired some concerns about inflation.

“I believe it is appropriate to monitor economic conditions and the outlook before making any further adjustments to the stance of policy,” Musalem said during a speech at the Economic Club of New York.

Fed Chair Jerome Powell also told lawmakers earlier this month that the Fed is not in a rush to adjust interest rates.

“With our policy stance now significantly less restrictive than it had been and the economy remaining strong, we do not need to be in a hurry to adjust our policy stance,” Powell said in testimony before the Senate Banking Committee.

The Fed will get a new look at inflation this Friday with the release of its preferred inflation gauge — the Personal Consumption Expenditures Index (PCE).

A separate measure, the Consumer Price Index (CPI), was hotter than expected for January.

It showed that consumer prices on a “core” basis, which strips out the more volatile costs of food and gas, climbed 0.4% over the prior month — higher than December’s 0.2% monthly gain and the largest monthly rise since April 2023.

Atlanta Federal Reserve president Raphael Bostic told Yahoo Finance last week that while interest rate cuts are still on the table this year, following the hotter-than-expected CPI reading from January, “I think the biggest question right now is whether that data point represents a new trend or just a bump in the road.”

Barkin argues that CPI isn’t as good a measure as PCE because it doesn’t account for substitutions as well.

If beef gets pricey and thus less popular, the PCE basket reflects that people move to an alternative, such as chicken. In contrast, the CPI is more static and is weighted more toward housing costs — which have been slow to come down.

“If headwinds persist, we may well need to use policy to lean against that wind,” said Barkin. “But for now, I take comfort in the significant drop of inflation from its peak and look forward to further progress.”

U.S. stocks struggled on Tuesday, with the S&P 500 and the Nasdaq touching one-month lows as a dour consumer confidence report put mounting economic uncertainties into sharp relief.

The S&P 500 and the Nasdaq both notched their fourth consecutive sessions in the red, while the Dow ended the day modestly higher.

“This is clearly a risk-off day and a continuation of a risk-off month,” said Peter Tuz, president of Chase Investment Counsel in Charlottesville, Virginia.

“Many companies are expressing caution about the direction of consumer spending at the moment and today’s consumer confidence number bears that out.”

The mood of the consumer, who props up about 70% of U.S. GDP, has dimmed considerably in February, according to The Conference Board’s consumer confidence index, which registered its steepest monthly drop since August 2021.

Rising consumer uncertainties were laid bare by an 11.3% plunge in the near-term expectations component, well below the level associated with impending recession, suggesting Americans are growing anxious about the potential negative economic impact of the policies of President Donald Trump’s administration.

Tuz said the political environment was not helping.

“Headlines have been pretty dramatic … and as a result consumers and maybe businesses are sitting on their hands to see how things shake out before making major purchasing decisions or other business decisions,” Tuz said.

“There are just lots of reasons to put off buying things today, including stocks.”

Survey data shows rising uncertainties

Richmond Federal Reserve President Tom Barkin said on Tuesday that current uncertainties call for a measured, cautious approach to monetary policy.

Interest-rate futures imply the U.S. Federal Reserve will hold its key interest rate steady for the first half of the year, according to data compiled by LSEG.

The CBOE market volatility index (.VIX), opens new tab, widely known as the “fear index,” spiked to its highest level since January 27.

Bitcoin , often viewed as a barometer of investor risk appetite, dropped 6.1%.

US stocks closed mixed on Tuesday as President Donald Trump’s revived tariff threats and potential toughening of China curbs weighed on market optimism while new data signaled fears over future economic growth.

Consumer confidence plummeted in February, notching its biggest monthly decline in nearly four years as 12-month inflation expectations jumped and recession fears escalated.

The tech-heavy Nasdaq Composite (^IXIC) finished the volatile trading day down around 1.3%, dragged down by shares of Magnificent Seven players like Nvidia (NVDA) and Tesla (TSLA). The benchmark S&P 500 (^GSPC) dropped roughly 0.4%, while the Dow Jones Industrial Average (^DJI) reversed earlier session declines to end the day in the green, up about 0.4%.

Some of the biggest market moves also came from the cryptocurrency space, where the price of bitcoin (BTC-USD) tumbled below $90,000 for the first time since November.

Bitcoin touched a low closer to $86,000 in the early morning hours, its lowest level since early November. Prices stabilized to just around $88,000 at the market close.

Meanwhile, the price of ether (ETH-USD), the world’s second-largest cryptocurrency, fell around 6% to just over $2,500, bouncing off of its session lows. Crypto-related stocks, including Coinbase (COIN) and Strategy (MSTR), were also under pressure throughout the trading day.

Trump’s signal that his trade overhaul isn’t over has unsettled markets wondering about the impact on growth prospects. Investors are parsing his brief comment that tariffs on Mexico and Canada will go forward next week.

The benchmark 10-year Treasury yield (^TNX) fell to its lowest level this year, around 4.3%, amid growing belief that tariffs will weaken the US economy. That prompted traders to bump up bets on interest rate cuts.

At the same time, his administration is said to be pursuing tougher chip curbs on China, after Trump issued a directive to limit investments between the US and the top trading partner. AI chip giant Nvidia’s (NVDA) stock was in focus with its highly anticipated earnings due Wednesday. The company is already facing headwinds from tariffs and export controls.

Elsewhere, Tesla stock (TSLA) fell more than 8% Tuesday after the electric vehicle maker reported sales in Europe dropped 45% in January.

Advertising and marketing company Zeta Global (NYSE:ZETA) announced better-than-expected revenue in Q4 CY2024, with sales up 49.6% year on year to $314.7 million. Revenue guidance for the full year exceeded analysts’ estimates, but next quarter’s guidance of $254 million was less impressive, coming in 1.2% below expectations. Its GAAP profit of $0.06 per share was $0.02 above analysts’ consensus estimates.

Zeta (ZETA) Q4 CY2024 Highlights:

Revenue: $314.7 million vs analyst estimates of $295 million (49.6% year-on-year growth, 6.7% beat)

EPS (GAAP): $0.06 vs analyst estimates of $0.04 ($0.02 beat)

Adjusted EBITDA: $70.38 million vs analyst estimates of $65.84 million (22.4% margin, 6.9% beat)

Management’s revenue guidance for the upcoming financial year 2025 is $1.24 billion at the midpoint, beating analyst estimates by 2.4% and implying 23.3% growth (vs 37% in FY2024)

EBITDA guidance for the upcoming financial year 2025 is $256.5 million at the midpoint, above analyst estimates of $241 million

Operating Margin: 2.2%, up from -15.1% in the same quarter last year

Free Cash Flow Margin: 6.2%, down from 9.6% in the previous quarter

Market Capitalization: $5.14 billion

“At Zeta, we’ve consistently skated to where the puck is going. Our early investments in AI and first-party data are resonating with customers and prospects, fueling our record fourth quarter results and contributing to our market share gains,” said David A. Steinberg, Co-Founder, Chairman, and CEO of Zeta.

Company Overview

Co-founded by former Apple CEO John Sculley, Zeta Global (NYSE:ZETA) provides software and data analytics tools that help companies market their products to billions of customers.

Advertising Software

The digital advertising market is large, growing, and becoming more diverse, both in terms of audiences and media. As a result, there is a growing need for software that enables advertisers to use data to automate and optimize ad placements.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Zeta’s 29.9% annualized revenue growth over the last three years was impressive. Its growth beat the average software company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Zeta Quarterly Revenue

This quarter, Zeta reported magnificent year-on-year revenue growth of 49.6%, and its $314.7 million of revenue beat Wall Street’s estimates by 6.7%. Company management is currently guiding for a 30.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 20.2% over the next 12 months, a deceleration versus the last three years. Still, this projection is noteworthy and suggests the market sees success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Zeta is extremely efficient at acquiring new customers, and its CAC payback period checked in at 1.4 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Zeta more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

Key Takeaways from Zeta’s Q4 Results

We were impressed by Zeta’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also glad its full-year EBITDA guidance trumped Wall Street’s estimates. On the other hand, its revenue guidance for next year suggests a significant slowdown in demand and its revenue guidance for next quarter fell slightly short of Wall Street’s estimates. Overall, we think this was still a decent quarter with some key metrics above expectations. The market seemed to focus on the negatives, and the stock traded down 7.3% to $19.10 immediately after reporting.

Is Zeta an attractive investment opportunity right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

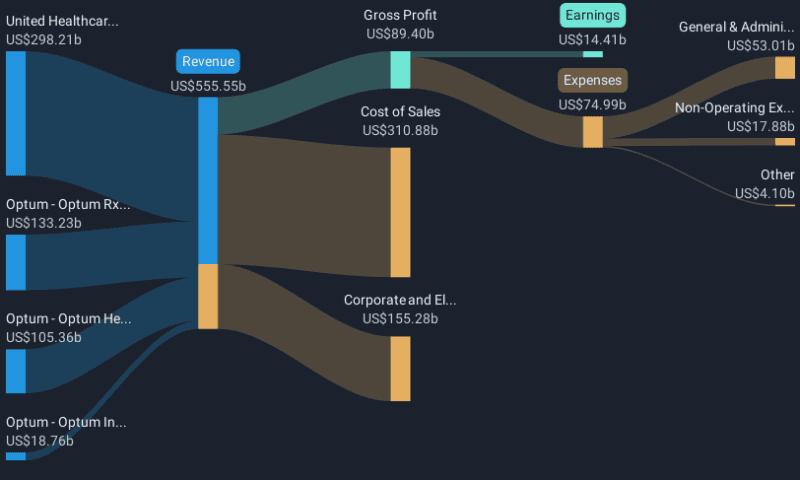

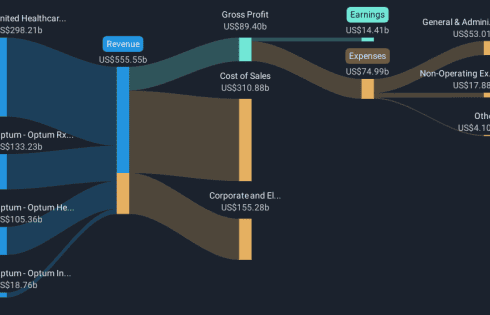

UnitedHealth Group (NYSE:UNH) experienced a share price decline of 11% over the past week, amid a mixed landscape for major U.S. stock indexes grappling with a broader market downturn. The announcement of a $2.10 cash dividend, set to be paid in March 2025, was among the key events during this period, potentially impacting investor sentiment due to its financial implications. As the Dow Jones recorded its worst week since October last year and tech stocks faced significant pressure, UnitedHealth Group was not immune to these market forces. Notably, the Dow managed a slight recovery of 0.2%, but the overall tech and healthcare segments remained under stress, influencing UNH’s recent performance. The decline aligns with a period where investors are keeping a keen eye on upcoming economic indicators, possibly fueling volatility and affecting risk assessment across various sectors.

Despite the recent week’s challenges, UnitedHealth Group (NYSE:UNH) has shown resilient growth over the last five years, achieving a total shareholder return of 83.80%. Even so, over the past year, the company underperformed against the US Healthcare industry and the broader US market. A key influencer was an $8.3 billion one-off loss reported in December 2024, impacting earnings. Additionally, legal challenges, including a class action lawsuit in January 2024 over their acquisition of Change Healthcare, may have affected investor confidence.

In September 2022, UnitedHealth’s partnership with Walmart to expand healthcare services highlighted a proactive expansion strategy, which could have positively influenced its longer-term returns. Despite these efforts, the company’s high price-to-earnings ratio compared to peers suggests a relative overvaluation within the industry, possibly weighing on investor sentiment. These elements collectively paint a comprehensive picture of UnitedHealth’s share performance over recent years, reflecting both growth initiatives and challenges faced in the marketplace.