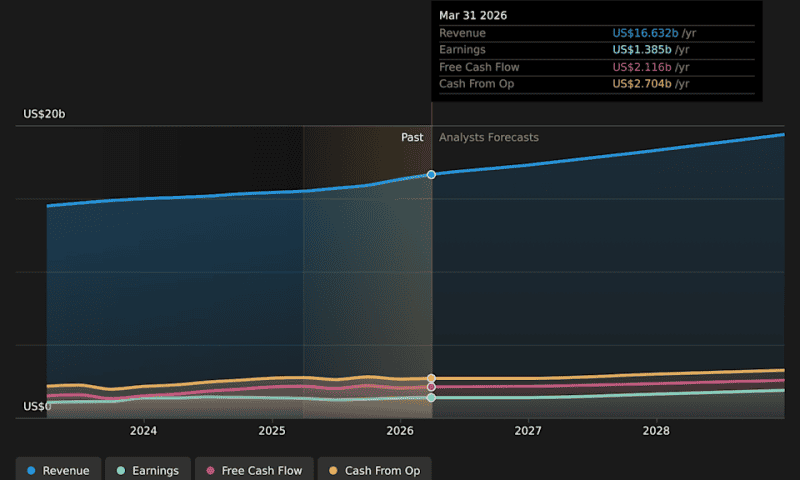

Oracle (NYSE:ORCL) Valuation Check After AI Readthrough From Snowflake And Dell Earnings

Oracle (ORCL) has been pulled into the recent AI-driven rally, with its stock reacting to…

Oracle (NYSE:ORCL) Valuation Check After AI Readthrough From Snowflake And Dell Earnings

Oracle (NYSE:ORCL) Valuation Check After AI Readthrough From Snowflake And Dell Earnings A Look At Super Group (NYSE:SGHC) Valuation After Recent Share Price Weakness

A Look At Super Group (NYSE:SGHC) Valuation After Recent Share Price Weakness Dollar steady as markets await progress on Middle East peace talks

Dollar steady as markets await progress on Middle East peace talks New Fed Chair Kevin Warsh Has Big Plans. They Could End the Trump Bull Market.

New Fed Chair Kevin Warsh Has Big Plans. They Could End the Trump Bull Market. The Iran War’s First 90 Days Upended Energy Markets

The Iran War’s First 90 Days Upended Energy Markets South Korea stocks hit fresh high amid mixed regional trade despite Trump’s Iran deal caution

South Korea stocks hit fresh high amid mixed regional trade despite Trump’s Iran deal caution Berkshire buys Taylor Morrison for $6.8 billion. Buffett touts Abel’s dealmaking

Berkshire buys Taylor Morrison for $6.8 billion. Buffett touts Abel’s dealmaking UAW declares midnight strike at American Axle, a key GM supplier

UAW declares midnight strike at American Axle, a key GM supplier Is It Too Late To Consider Buying IQVIA Holdings Inc. (NYSE:IQV)?

Is It Too Late To Consider Buying IQVIA Holdings Inc. (NYSE:IQV)? GameStop (NYSE: GME) And eBay (NASDAQ: EBAY) Takeover Bid Takes Center Stage At Princeton Corporate Governance Forum

GameStop (NYSE: GME) And eBay (NASDAQ: EBAY) Takeover Bid Takes Center Stage At Princeton Corporate Governance Forum