Wall Street ends higher after Zelenskiy and Trump clash

The average rate on a 30-year mortgage in the U.S. eased for the sixth week in a row, a welcome boost in purchasing power for home shoppers just as the annual spring homebuying season gets going.

The average rate fell 6.76% from 6.85% last week, mortgage buyer Freddie Mac said Thursday. A year ago, it averaged 6.94%.

Borrowing costs on 15-year fixed-rate mortgages, popular with homeowners seeking to refinance their home loan to a lower rate, also eased this week. The average rate fell to 5.94% from 6.04% last week. A year ago, it averaged 6.26%, Freddie Mac said.

The steady decline in mortgage rates rates this year hasn’t been enough to change the affordability equation for many prospective home shoppers, especially first-time buyers who don’t have equity from an existing home to put toward a new home purchase.

Sales of previously occupied U.S. homes fell in January as rising mortgage rates and prices froze out many would-be homebuyers despite a wider selection of properties on the market.

New data on pending home sales, a bellwether for future completed sales, point to potentially further sales declines in coming months. They slid to an all-time low in January.

The average rate on a 30-year mortgage is now at its lowest level since Dec. 19, when it was also 6.72%. It briefly fell to a 2-year low last September, but has been mostly hovering around 7% this year. That’s more than double the 2.65% record low the average rate hit a little over four years ago.

“The drop in mortgage rates, combined with modestly improving inventory, is an encouraging sign for consumers in the market to buy a home,” said Sam Khater, Freddie Mac’s chief economist.

The inventory of U.S. homes on the market climbed last month to its highest level since June 2020, according to data from Redfin. But mortgage rates and prices remain an unaffordable combination for many would-be homebuyers.

Mortgage rates are influenced by several factors, including how the bond market reacts to the Federal Reserve’s interest rate policy decisions.

The latest pullback in rates echoes a decline in the 10-year Treasury yield, which lenders use as a guide for pricing home loans.

The yield, which was at 4.79% in mid-January, has been mostly easing since then, reflecting worries among bond investors over the potential impact from tariffs and other policies proposed by the Trump administration.

The 10-year yield was at 4.28% in midday trading Thursday.

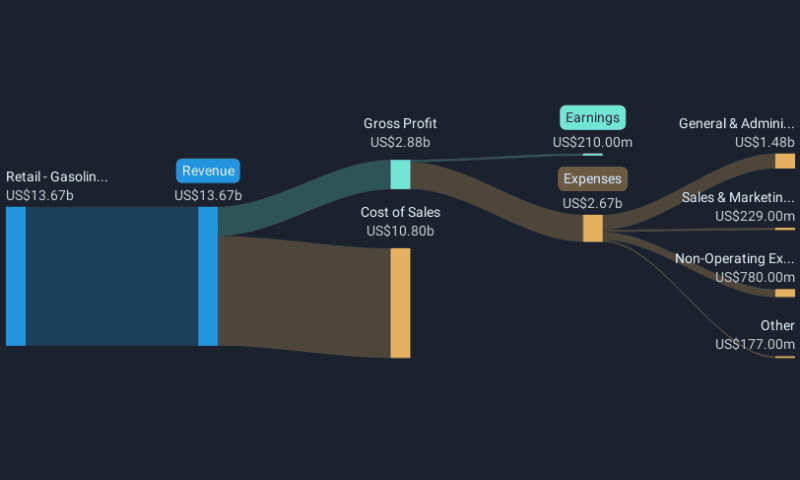

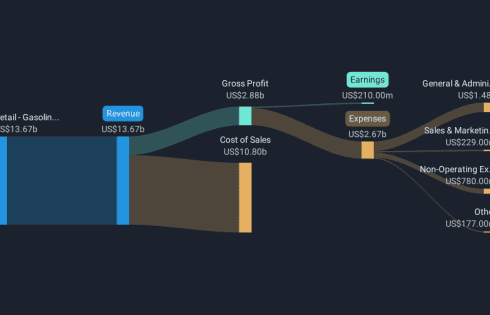

Carvana (NYSE:CVNA) recently announced its fourth quarter and full year earnings, showing significant growth in sales and a return to profitability with a net income of $79 million after a previous loss. However, the net income for the full year was $210 million, a decline from the previous year’s $450 million, which may have influenced investor sentiment. Alongside these financial results, Carvana’s filing of a shelf registration for $660 million in Class A Common Stock might have raised concerns about future share dilution among shareholders. These company-specific developments occurred against a backdrop of mixed market performance, as the broader U.S. stock market experienced fluctuations amid tariff announcements and tech stock volatility. The overall market dip of 3.6% over the past month was mirrored by Carvana’s share price decreasing by 3.93%, reflecting broader market uncertainties and company-specific challenges during this period.

Carvana’s shares delivered a remarkable total return of 208.24% over the last year. During this period, the company’s stock outperformed both the US market, which saw a 16.9% return, and the specialty retail industry, which achieved a 9.1% return. Several key events contributed to this performance. In July 2024, Carvana expanded its market reach by offering same-day vehicle delivery services in regions such as Las Vegas, Houston, and Kansas City. This strategic expansion helped cater to a broader customer base, potentially enhancing revenue streams.

Moreover, the company’s integration into the Russell 1000 Index on July 1, 2024, may have positively influenced investor perceptions, attracting more institutional attention. Earnings announcements throughout the year, including a swing to profitability with a US$79 million net income in Q4 2024, further strengthened investor confidence. However, the filing of a shelf registration in February 2025 for US$660 million in common stock hinted at potential future dilution, possibly tempering enthusiasm among some investors.

Aerospace and defense company HEICO (NSYE:HEI) reported Q4 CY2024 results topping the market’s revenue expectations , with sales up 14.9% year on year to $1.03 billion. Its GAAP profit of $1.20 per share was 26.6% above analysts’ consensus estimates.

Is now the time to buy HEICO? Find out in our full research report.

Revenue: $1.03 billion vs analyst estimates of $977.6 million (14.9% year-on-year growth, 5.4% beat)

EPS (GAAP): $1.20 vs analyst estimates of $0.95 (26.6% beat)

Adjusted EBITDA: $273.9 million vs analyst estimates of $251.6 million (26.6% margin, 8.9% beat)

Operating Margin: 22%, up from 20.1% in the same quarter last year

Free Cash Flow Margin: 18%, up from 11% in the same quarter last year

Market Capitalization: $27.97 billion

Founded in 1957, HEICO (NYSE:HEI) manufactures and services aerospace and electronic components for commercial aviation, defense, space, and other industries.

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, HEICO’s sales grew at an exceptional 13.8% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. HEICO’s annualized revenue growth of 30.6% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, HEICO reported year-on-year revenue growth of 14.9%, and its $1.03 billion of revenue exceeded Wall Street’s estimates by 5.4%.

Looking ahead, sell-side analysts expect revenue to grow 7.8% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is above average for the sector and implies the market is baking in some success for its newer products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

HEICO has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 21.4%.

Looking at the trend in its profitability, HEICO’s operating margin rose by 1.5 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, HEICO generated an operating profit margin of 22%, up 1.9 percentage points year on year. This increase was a welcome development and shows it was recently more efficient because its expenses grew slower than its revenue.

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

HEICO’s EPS grew at a decent 8.4% compounded annual growth rate over the last five years. Despite its operating margin expansion during that time, this performance was lower than its 13.8% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

Diving into the nuances of HEICO’s earnings can give us a better understanding of its performance. A five-year view shows HEICO has diluted its shareholders, growing its share count by 2.2%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For HEICO, its two-year annual EPS growth of 24.9% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q4, HEICO reported EPS at $1.20, up from $0.82 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects HEICO’s full-year EPS of $4.04 to grow 9.8%.

Revenue, EBITDA, and EPS all beat by pretty convincing amounts this quarter. Zooming out, we think this was a solid quarter. The stock traded up 6.7% to $242.99 immediately after reporting.

HEICO put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.

Here’s what could soon cost you a lot more because of Trump’s massive tariffs

Here’s what could soon cost you a lot more because of Trump’s massive tariffs Federal Reserve is unlikely to rescue markets and economy from tariff turmoil anytime soon

Federal Reserve is unlikely to rescue markets and economy from tariff turmoil anytime soon Dow tumbles more than 1,600 the day after Trump’s major tariff announcement

Dow tumbles more than 1,600 the day after Trump’s major tariff announcement Stem (NYSE:STEM) Slips 12% In One Week Amid Financial Headwinds

Stem (NYSE:STEM) Slips 12% In One Week Amid Financial Headwinds Japan stocks extend declines as Trump tariffs roil markets, Nikkei falls over 3%

Japan stocks extend declines as Trump tariffs roil markets, Nikkei falls over 3% More homes are finally hitting the spring market. Will buyers take the plunge?

More homes are finally hitting the spring market. Will buyers take the plunge? Import tax on coffee pressures US roasters already facing high prices

Import tax on coffee pressures US roasters already facing high prices Musk to remain ‘friend and adviser’ to Trump after leaving Doge, says Vance

Musk to remain ‘friend and adviser’ to Trump after leaving Doge, says Vance Trump to weigh options for potential TikTok deal, sources say, with ban days away

Trump to weigh options for potential TikTok deal, sources say, with ban days away Study reveals key reasons young people fail to save for retirement

Study reveals key reasons young people fail to save for retirement