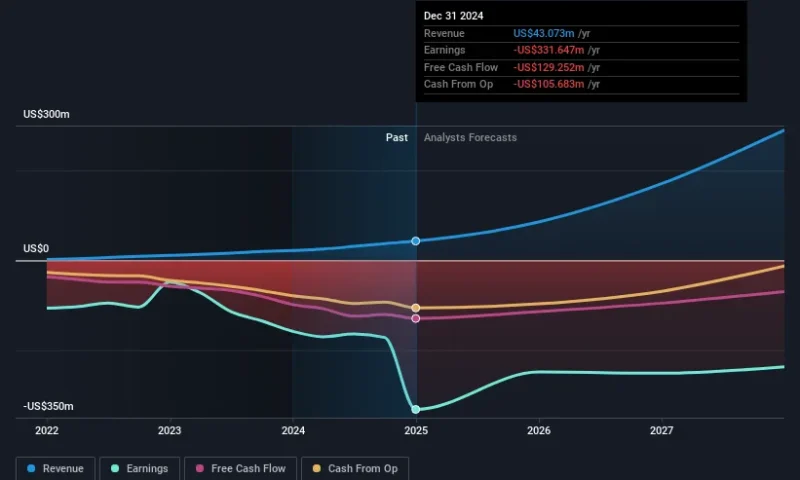

One of the biggest stories of last week was how IonQ, Inc. (NYSE:IONQ) shares plunged 23% in the week since its latest yearly results, closing yesterday at US$24.57. Revenues of US$43m beat expectations by a respectable 4.0%, although statutory losses per share increased. IonQ lost US$1.56, which was 80% more than what the analysts had included in their models. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there’s been a strong change in the company’s prospects, or if it’s business as usual. We’ve gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

Following the latest results, IonQ’s five analysts are now forecasting revenues of US$85.4m in 2025. This would be a substantial 98% improvement in revenue compared to the last 12 months. The loss per share is expected to greatly reduce in the near future, narrowing 25% to US$1.15. Before this latest report, the consensus had been expecting revenues of US$83.2m and US$0.95 per share in losses. While this year’s revenue estimates increased, there was also a very substantial increase in loss per share expectations, suggesting the consensus has a bit of a mixed view on the stock.

Spiting the revenue upgrading, the average price target fell 5.5% to US$44.60, clearly signalling that higher forecast losses are a valuation concern. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company’s valuation. There are some variant perceptions on IonQ, with the most bullish analyst valuing it at US$54.00 and the most bearish at US$29.00 per share. This shows there is still a bit of diversity in estimates, but analysts don’t appear to be totally split on the stock as though it might be a success or failure situation.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It’s clear from the latest estimates that IonQ’s rate of growth is expected to accelerate meaningfully, with the forecast 98% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 67% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 6.7% per year. Factoring in the forecast acceleration in revenue, it’s pretty clear that IonQ is expected to grow much faster than its industry.

The Bottom Line

The most important thing to note is the forecast of increased losses next year, suggesting all may not be well at IonQ. Happily, they also upgraded their revenue estimates, and are forecasting them to grow faster than the wider industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.