A strong U.S. dollar has been a vital — if often overlooked — source of support for U.S. stocks since the 2008 financial crisis. But this could soon change as the greenback enters a prolonged period of weakness, according to a top Morgan Stanley strategist.

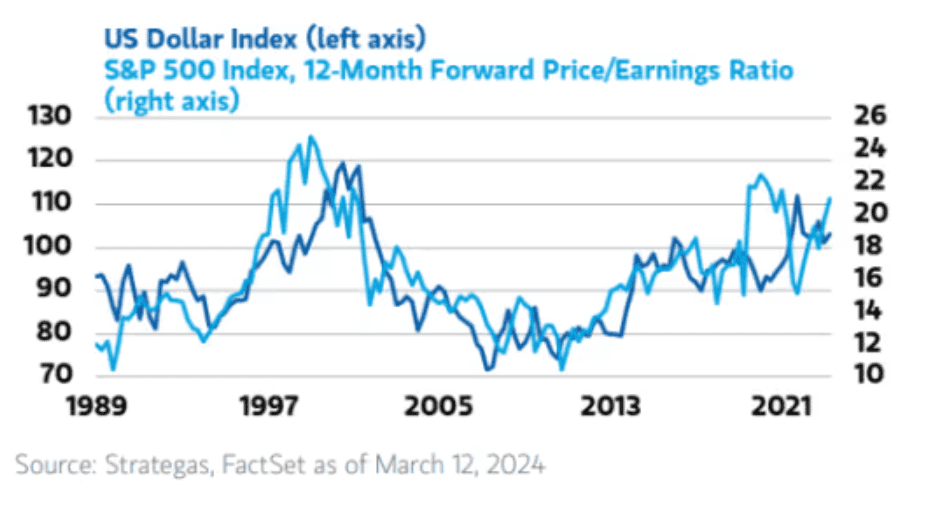

Over time, a stronger greenback has been correlated with rising equity valuations, as the chart below illustrates.

Of course, there have been exceptions. In 2022, the dollar soared as international investors sought safety in the greenback amid a wave of inflation — the worst in 40 years — that hammered global stocks and bonds.

But a persistently weaker dollar would leave the U.S. more prone to a stagflation-like scenario where the U.S. economy sees tepid growth and stubborn inflation — the opposite of the “goldilocks” scenario that has helped bolster U.S. equities over the past year, said Morgan Stanley Wealth Management Chief Investment Officer Lisa Shalett.

And signs that this “regime shift” is already under way have multiplied recently, Shalett said in a recent report for Morgan Stanley clients shared with MarketWatch.

The Bank of Japan’s decision late Monday to raise interest rates and loosen its grip on domestic markets is one such development.

Although the Japanese yen USDJPY, 0.23% weakened against the buck on Tuesday, the BoJ’s decision to start tightening monetary policy while other global central banks are preparing to cut interest rates will likely boost the yen over time, helping to reverse some of its steep losses against the buck over the past two years, market strategists said.

Shalett said the BoJ decision could inspire Japanese investors to repatriate money invested overseas, removing a crucial source of support for U.S. stocks and bonds.

China represents another threat, as burgeoning geopolitical tensions could accelerate de-dollarization, weakening the buck’s grip on international trade and finance.

Meanwhile, rising prices of gold, bitcoin and other commodities suggest the dollar could weaken further in the months ahead.

The ICE U.S. Dollar Index DXY, which gauges the dollar’s strength against a basket of rivals, shed 3% in 2023. But after a strong start to 2024, the buck’s advance stalled in March, even as investors continued to dial back expectations for Fed interest-rate cuts. It is down 0.3% so far this month, FactSet data show.

While this may not seem like much, this weakness suggests that favorable interest-rate differentials, long cited as the most reliable driver of dollar strength, may no longer be enough to support the U.S. currency, Shalett said.

Furthermore, gold’s recent ascent to record highs suggests that China may be increasingly diversifying its reserves away from the dollar and into the yellow metal — a trend that could continue.

Investors looking to insulate their portfolios from this risk should consider buying international stocks, Shalett said. She recommended Japan, Mexico, Brazil and India as suitable alternatives to the U.S.

Investing in more real assets, including cyclical commodities like crude oil and copper, as well as safe assets like gold, could also help investors profit from a weaker dollar. Finally, within their U.S. stock portfolios, investors should consider shifting more exposure to REITs, which have underperformed the broader stock market lately.

While a rising greenback has helped boost U.S. stocks since 2008, the trend went into overdrive following the start of the COVID-19 pandemic.

Over the past few years, the buck has found itself at the heart of the Federal Reserve’s easy-money regime, which has persisted despite the Fed’s aggressive interest-rate hikes and shrinking of its Treasury holdings.

Recently, the strong buck has helped boost stocks by helping to combat inflation, weighing on prices of imports and commodities. Its role as the indispensable global currency has also helped to support demand for Treasurys, blunting the impact of rising U.S. budget deficits that many investors fear could lead to a deluge of debt issuance that could overwhelm demand.

Rising long-term Treasury yields are frequently cited as a potential threat to stock valuations, and recent lows in stocks coincided with the highest yields in more than 16 years.

Shalett said 100% of the decline in inflation in the U.S. over the past two years can be attributed to the strong dollar. The buck has gained nearly 6% in that time, based on the performance of the dollar index.

For now, the dollar appears to still be on strong footing, trading higher on Tuesday while U.S. stocks opened mostly lower. The dollar index was up 0.5% at 103.90, while the S&P 500 SPX was off by 0.3% at 5,133. The Nasdaq Composite COMP was off by 0.9% at 15,959, while the Dow Jones Industrial Average DJIA traded higher, up 63 points, or 0.2%, at 38,850.