More analysts are ‘neglecting to mention valuations at all in making their cases for the market,’ says Leuthold Group’s CIO

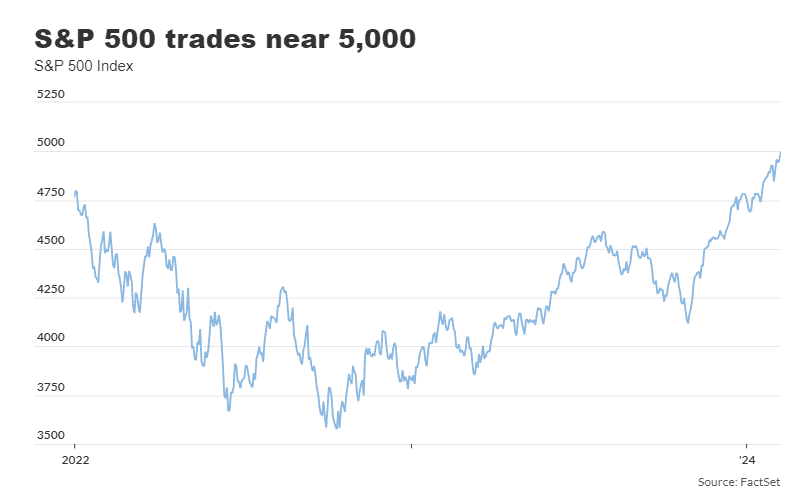

The U.S. stock market appears more “accident prone” because of high valuations, as the S&P 500 index nears its 5,000 milestone, according to Leuthold Group.

The S&P 500, a gauge of large-cap stocks in the U.S., ended just shy of 5,000 on Wednesday, while notching another record close this year, according to FactSet data. The index SPX gained 0.8%, ending at 4,995.06.

“Increasingly, we notice evermore analysts neglecting to mention valuations at all in making their cases for the market,” Doug Ramsey, chief investment officer at Leuthold, said in a note Wednesday. “And it is not just market bulls who are doing so,” he said. “Persistently high equity valuations are something to which most investors now seem to be inured.”

The S&P 500 has notched a series of all-time peaks so far in 2024, after in January closing at its first record high in about two years. The index has been rising against the backdrop of a growing U.S. economy, easing inflation and investor optimism surrounding artificial intelligence.

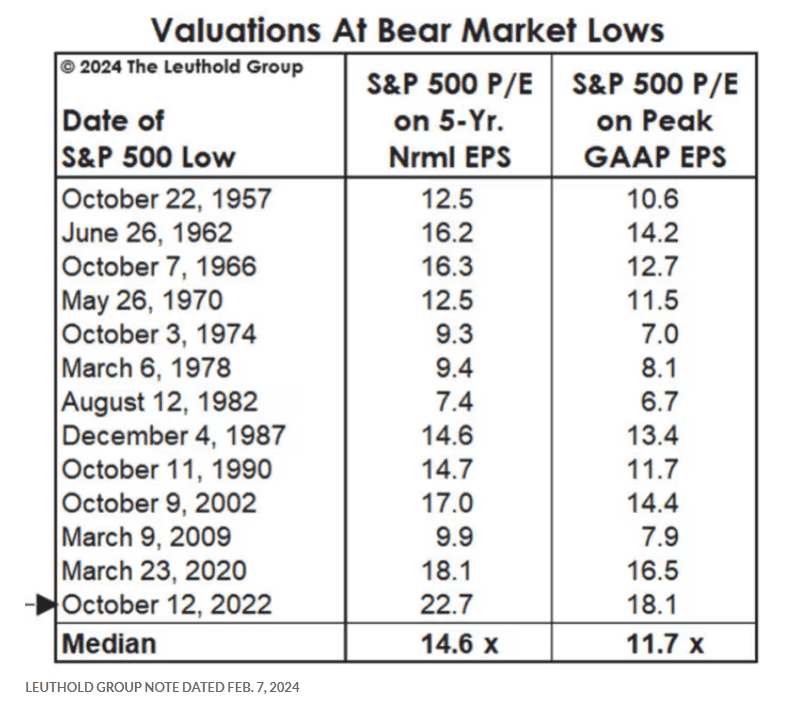

The current bull market follows an October 2022 bottom that was “the priciest bear market low in history—and by a long shot,” according to the Leuthold note.

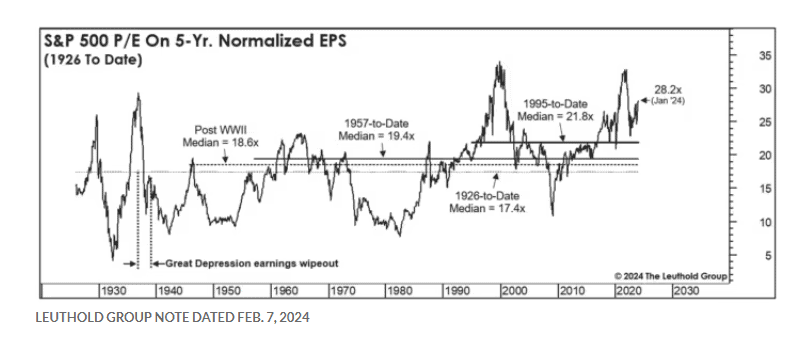

The S&P 500’s five-year normalized price-to-earnings ratio was 22.7x at the 2022 low, “roughly 25% above the 18.1x seen at the depths of the COVID collapse,” said Ramsey. More recently, the S&P 500’s P/E ratio on five-year normalized earnings per share, or EPS, was at 28.2x in January, according to the note.

Meanwhile, the S&P 500 current valuation appears stretched at a price-to-earnings ratio of more than 20 times forward earnings estimates, according to Bob Doll, chief executive officer and chief investment officer of Crossmark Global Investments.

Many investors appear to think that a “soft landing is in the bag” for the U.S. economy as the Fed keeps up its effort at bringing inflation down to its 2% target, he said by phone. But it’s “not so easy.”

To Doll’s thinking, “you can’t have it both ways,” in expecting both double-digit earnings growth for the S&P 500 in 2024 and six interest-rate cuts by the Fed this year.

Traders in the federal-funds futures market are indicating potentially five or more rate cuts by yearend, based on reductions of a quarter percentage point each time, according to the CME FedWatch tool on Wednesday afternoon, at last check.

But in Doll’s view, it would take an economic slowdown for the Fed to cut rates six times, and that many cuts alongside earnings growth of around 12% seems like “nirvana.”

Also, it may be tough for the Fed to lower rates in a good economy with such above-average growth in company earnings, according to Doll. He said he’s monitoring wage growth in the so far resilient U.S. labor market as an area that risks keeping upward pressure on inflation.

Inflation is probably a “little more sticky than people think,” he said.

Doll said he anticipates that the Fed may reduce its benchmark rate only as many as three times this year, potentially disappointing the market, while also worrying that lagging effects from the Fed’s monetary tightening via rate hikes may still slow the economy.

“Whether or not there’s a recession in 2024 is a critical call,” Ramsey said in the Leuthold note.

But “consider that the last 5-1/2 years have seen three ‘major declines’ in the S&P 500 (and significantly deeper losses for other indexes), despite the economy having been in recession for just two months out of that entire span,” Ramsey wrote. “Stock market risks would be higher even if one ignored nearly two years of Fed tightening.”

The S&P 500 has climbed 4.7% so far this year through Wednesday, driven by gains in so-called Big Tech stocks such as Nvidia Corp. NVDA, +2.75%, Meta Platforms Inc. META, +3.27%, Amazon.com Inc. AMZN, +0.82% and Microsoft Corp. MSFT, +2.11%, according to FactSet data, at last check.

For Doll, the excitement around AI appears too “hyped.” While he holds some tech stocks, he said he owns less of those with high valuations. International Business Machines Corp. IBM, +0.18% is an example of tech stock that provides some exposure to AI but with a more attractive valuation, according to Doll.

“In past tech cycles like the dotcom era, it was all about disruptors—new young companies eating away at market share,” Solita Marcelli, CIO for the Americas at UBS Global Wealth Management, said in an investment research note earlier this month. “With AI, incumbents are currently in the best position.”