Third-party foundry prospects are still ‘dismal,’ Citi analyst says

Once in Wall Street’s doghouse, Intel Corp.’s stock is now a hedge-fund favorite, but a Citi analyst thinks a number of factors need to go right in order for the shares to really work.

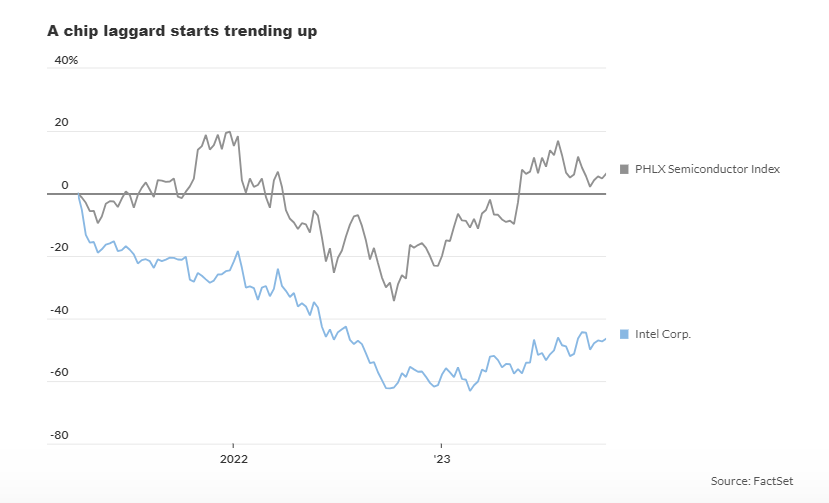

Intel’s stock INTC, +1.64% was one of the most popular names discussed at recent investor meetings held by Citi Research analyst Christopher Danely, which might have been a surprising feat a few years ago: Intel shares had shed 61% from their April 2021 peak to the end of 2022, far outpacing losses for the PHLX Semiconductor Index SOX over that span, although they’re up 38% so far this year, essentially in line with the index.

“We get a sense that some investors are positive on Intel based on the company regaining the lead in manufacturing and success in foundry,” Danely said in a recent note that summarized his investor meetings.

While its 7 and 4 nodes are already being manufactured, Intel’s 3 node is expected out before the end of the year, the 20A node is expected out in the first half of 2024 and the 18A is expected out in the second half of 2024. Intel used to name chips according to the size of their increasingly small transistors, but more than two years ago it switched to a new type of nomenclature, while competitors still use nanometers, or nm.

Back in July 2020, Intel’s status as chip leader began crumbling as the company, then led by Bob Swan, announced that its next generation of chips, 7-nm, would be delayed, putting the company behind Advanced Micro Devices Inc. AMD, +1.30%, which was already selling a 7-nm chip at the time.

Danely isn’t yet sold on Intel’s stock, which he rates at neutral with a $34 price target, but he said the once-undisputed chip leader could make a comeback if it makes almost no mistakes for more than a year.

Shares are still somewhat volatile. Having logged their longest winning streak in nearly three years in September, Intel shares were also the worst performer on the Dow Jones Industrial Average DJIA two days running as the company held an AI-product event. They had a similar two-day run during a foundry-services event over the summer.

“If Intel executes on its five nodes in four years manufacturing roadmap — we believe it will result in them regaining leadership products in the server end market and ultimately get the company gross margins somewhere in the low to mid 50% range and [earnings per share] in the $3.00-$4.00 range which could translate to a $50-$60 stock and would be enough for us to become more positive in our rating,” Danely wrote.

Of the 43 analysts surveyed by FactSet, eight have buy ratings on the stock, 28 have hold-grade ratings and seven have sell ratings, along with an average price target of $36.50.

Essentially, the Citi analyst thinks the company needs near-flawless execution, something Intel has struggled with for more than three years. Shares bottomed earlier this year after the company reported a quarterly loss of $2.76 billion, its largest quarterly loss on record.

Danely is still “very skeptical [about] whether Intel can achieve success in foundry,” but he believes that it “has a chance to regain the manufacturing lead, which could cause our rating to become positive.” Getting there would require “zero delays in manufacturing for another few quarters,” at which point Danely would “become confident Intel can execute its aggressive roadmap,” he said.

Intel is trying to compete with third-party foundry giants like Taiwan Semiconductor Manufacturing Co. TSM, +0.84%, Samsung Electronics Co. 005930, 3.27% and SK Hynix Inc. 000660, 4.67% through its Intel Foundry Service business, but Danely wrote over the summer that he viewed this as a “wrong move.”

Danely continues to believe Intel’s third-party foundry prospects “remain dismal.”