Recent ‘special rebalancing’ is unlikely to hurt the performance of the index or the stocks that are affected

The Nasdaq 100 Index’s “special rebalancing,” which took effect on July 24, is unlikely to have any noticeable effect on either the performance of the index itself or the individual stocks that are affected.

Nasdaq’s motivation behind this change was to address the “overconcentration” that had resulted from the growth of just six high-tech stocks into collectively representing more than 50% of the index’s combined market cap. The rebalancing reduced the collective index weight of those six — Microsoft MSFT, -3.76%, Apple AAPL, +0.45%, Alphabet GOOGL, +5.78%, Nvidia NVDA, -0.50%, Amazon.com AMZN, -0.76%, and Tesla TSLA, -0.35% — to 40%.

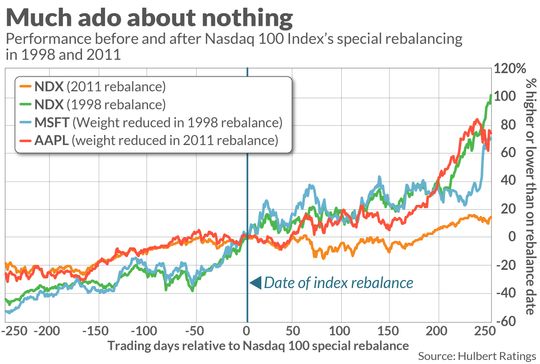

Many immediately predicted that this rebalance would be negative for these six stocks, on the grounds that hundreds of billions are invested in index funds benchmarked to the Nasdaq 100 NDX, -0.40%. But history doesn’t bear out their concern. Consider what happened the other two times when the Nasdaq 100 underwent a similar special rebalancing. The first was in December 1998, when Microsoft had grown to represent more than 25% of the market cap of the entire index. After the rebalance, Microsoft’s index weight was significantly lower.

By the same logic employed by those worrying about this year’s rebalance, Microsoft should have suffered. Instead, over the 12 months subsequent to that rebalance, Microsoft stock gained more than 70%.

A similar story is told by Apple’s stock following the Nasdaq 100’s special rebalance in 2011. In that year’s rebalance, Apple’s index weight was cut to 12% from more than 20%. Yet Apple shares rose more than 70% in the year following.

Furthermore, as you can see from the chart above, there was no noticeable impact of either the 1998 or the 2011 rebalances on the Nasdaq 100 itself. Its returns over the 12 months following those two rebalancings were not significantly different than they were over the 12 months prior.

Theories and realities

It’s difficult to draw confident conclusions from just two rebalancings, and it certainly seems plausible that an index that becomes too concentrated will be riskier. But such concerns are largely theoretical at this point rather than immediate causes for concern.

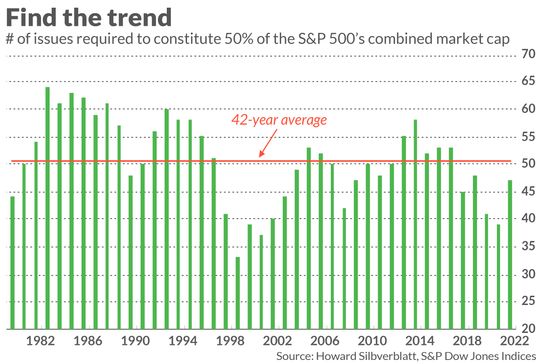

That’s because there’s little evidence that the stock market is systematically becoming more concentrated. You may find that surprising, given myriad headlines bemoaning increasing overconcentration. In fact, the long-term trend has remained steady.

This is illustrated by the chart below, which plots for each year since 1980 the number of stocks in the S&P 500 SPX, -0.02% required to constitute 50% of the index’s combined market cap. The year-end-2022 level is not significantly different than the four-decade average.

Another indication that concerns about overconcentration are overblown is the performance of the equal-weight version of the S&P 500. If the cap-weighted version of the index were becoming top-heavy, you’d expect to see a significant deviation between its performance and that of the equal-weight version. Such a gap hasn’t emerged, however.

In nine of the past 19 calendar years in which the Invesco S&P 500 Equal Weight ETF RSP, +0.23% has existed, the cap-weighted version (as represented by the SPDR S&P 500 SPY, +0.02% has come out ahead. It has lagged 11 times. Overall the two have performed remarkably similarly.

The bottom line? When assessing the outlook for the overall market or individual tech stocks, there are far more significant factors to take into account than the Nasdaq 100’s special rebalance.