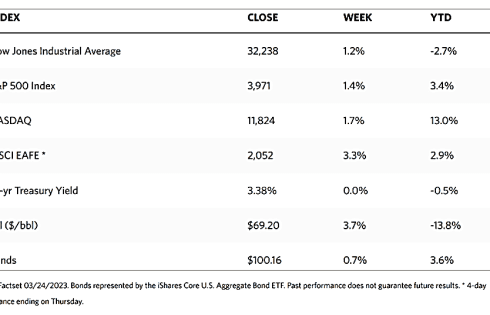

Stock Markets

The uncertainty in the U.S. regional and global banking system has, in just over two weeks, notably shifted the performance of financial markets and, most likely, the path of the Federal Reserve in its policies moving forward. According to the Wall Street Journal markets data, The major stock market indexes generally recovered over the week to recover the lost ground resulting from the shocks that occurred in the final industry during the preceding weeks. The Dow Jones Industrial Average is up by 1.18% and the total stock market was also ahead by 1.26%, whereas the transportation and utilities sectors underperformance among the other sectors. The S&P 500 Index likewise expanded by 1.39% and the Nasdaq Stock Market Composite advanced by 1.66%. The NYSE Composite gained by 1.09%. The CBOE Volatility Index fell by 14.78%, indicative of a drop in investors’ risk perception. Financials underperformed for a third straight week, however, and the small real estate sector took the brunt of consumer concerns about how stresses in the regional banking system would affect the commercial real market, where regional banks are the major lenders.

The Fed is now constrained to perform a balancing act between navigating the liquidity pool on the one hand and battling inflation with rate increases on the other. The policy-setting body is now compelled to consider pausing its interest-rate-hiking cycle, and the recent tightening in financial conditions resulting from the banking crisis may potentially slow economic activity and cool inflation. Many stock market investors who initially adopted a risk-on sentiment have lately shifted towards more defensive positioning, gravitating towards resilient sectors such as consumer staples, health care, and technology outperforming over the past month. Volatility may continue in the near term as investors shake off the fear and restore confidence in the banking sector, and opportunities may continue to present themselves in both equity and bond markets.

U.S. Economy

In the past week, the most closely watched event was the conclusion of the Federal Reserve’s policy meeting on Wednesday. The Fed raised official short-term rates by 25 basis points, as was generally expected, and officials may stop raising rates after one more hike in May. Fed Chair Jerome Powell’s post-meeting press conference reflected a change in tone that was driven more by forecast uncertainty rather than a strong conviction that a 5.0% to 5.25% fed funds target range (if a 25 bps rate increase were to be announced in May) would sufficiently restrict inflation to preclude further rate hikes after May. In response to questions, Powell confirmed that rate cuts were not expected this year.

The week’s economic data appeared to indicate that the economy still had significant strength, at least heading into what may be a possible banking crisis. Weekly jobless claims remained close to a five-decade low; meanwhile, last Friday’s release of the S&P Global’s Composite Index of both current services and manufacturing activity jumped from 50.1 to 53.3 (note that readings above 50 indicate expansion). This marks the fastest pace of private sector growth since last May 2022, with new orders moving higher for the first time since September. S&P Global’s chief economist observed that the data were “broadly consistent with the annualized gross domestic product (GDP) growth approaching 2%, painting a far more positive picture of economic resilience” than had been observed during the previous months.

Core capital goods orders, which exclude orders for aircraft and defense and which are often relied upon as an indicator of business investment, were also higher than expected upon their release by the Commerce Department on Friday. Such orders increased in February by 0.2%, beating a consensus estimate that indicated a decline of the same magnitude. The optimistic data provided support that lifted the yield on the benchmark 10-year U.S. Treasury note from a six-month intraday low on Friday morning, although the yield still finished modestly lower for the week.

Metals and Mining

After hitting a one-year high, the precious metals market is seeing some selling pressure as it undergoes some cooling down ahead of the weekend. Gold briefly transcended above $2,000 per ounce and while it has since given way to some correction, there still appears to be further bullish momentum to resume its upward trek. The forecast is for safe-haven demand to continue to provide buying support to move gold prices up. According to financial headlines, the recent banking shocks that have hinted at a further financial crisis are far from over. In Europe, fears of contagion have spread from Switzerland to Germany as Deutsche Bank, the nation’s largest lender, saw its biggest increase in credit default swaps since 2018. Credit default swaps are similar to insurance for investors, and payout if a company defaults on its loans. Before the bailout from UBS, credit default swaps for Credit Suisse ran as high as 1,194 basis points, suggesting that further shocks are still to come. Gold remains an attractive safe-haven asset.

Over the week, gold moved from its previous close at $1,989.25 to this week’s close at $1,978.21 per troy ounce, a slight correction of 0.55%. Silver advanced by 2.79% from its week-ago price of $22.60 to its closing price this week at $23.23 per troy ounce. Platinum moved up slightly from last week’s $978.95 to this week’s $984.30 per troy ounce, a gain of 0.55%. Palladium moved sideways for the week, from what was previously $1,423.30 to its new closing price of $1,422.00 per troy ounce, a slight correction by 0.09%. The three-month LME prices for base metals were generally higher for the week. Copper climbed from last week’s $8,518.00 to this week’s $9,031.00 per metric tonne, a gain of 6.02%. Zinc began at $2,857.50 and ended at $2,907.00 per metric tonne, an increase of 1.73%. Aluminum climbed by 2.58% from $2,267.50 to $2,326.00 per metric tonne. Tin advanced from the previous week at $22,218.00 to this week at $24,348.00 per metric tonne for a gain of 9.59%.

Energy and Oil

Oil prices survived the financial jolts of the previous weeks and have rebounded marginally in the past week. ICE Brent climbed closer to $75 per barrel once more as the perennial bulls began to channel the commodity supercycle again. At the other end is the UN once more publishing yet another report of a “ticking climate bomb.” There were brief hopes that for at least a short amount of time, the price of fuel would once again be ideally determined by supply and demand, but this appears a fleeting prospect as Fed policy may soon influence again the movement of currencies and, again, the price of fuels and energy. In the meantime, as of Tuesday, U.S. crude exports are set for an all-time high this month, with outflows to Europe averaging 2.1 million barrels per day so far. Wide discounts for the WTI benchmark and a significantly lower domestic refining pull continue to incentivize oil producers to export as much as they can. Also in the news are reports that the G7 group is not seeking to revise the $60 per barrel price cap on Russian oil this week, three months after it took effect on December 5. Apparently, there is little appetite among members to introduce any modifications to the policy.

Natural Gas

On news regarding natural gas, the European Commission proposed an extension of gas consumption mandates for EU member states to have gas demand cut by 15% for another 12 months, with the knowledge that natural gas markets remain tight despite the exceptionally warm winter. For the week starting Wednesday, March 15, and ending Wednesday, March 22, 2023, the Henry Hub spot price fell $0.40 from $2.44 per million British thermal units (MMBtu) at the start of the week to $2.04/MMBtu at the week’s end. The price of the April 2023 NYMEX contract decreased by $0.268, from $2.439/MMBtu on March 15 to $2.171/MMBtu on March 22. The price of the 12-month strip averaging April 2023 through March 2024 futures contracts declined by $0.133 to $3.046/MMBtu.

International natural gas futures prices decreased for this report week. The weekly average front-month futures prices for liquefied natural gas (LNG) cargoes in East Asia fell by $0.98 to a weekly average of $13.24/MMBtu. Natural gas futures for delivery at the Title Transfer Facility in the Netherlands, the most liquid natural gas market in Europe, fell by $1.43 to a weekly average of $13.14/MMBtu. In the week last year corresponding to this week, (i.e., the week ending March 23, 2022), the prices were $34.83/MMBtu and $33.81/MMBtu in East Asia and at the TTF, respectively.

World Markets

European equities climbed this week despite weakness in bank stocks. The pan-European STOXX Europe 600 Index closed marginally higher (0.87%), as did the major stock indexes in the region. Italy’s FTSE mib advanced by 1.56%, Frances’ CAC 40 Index climbed by 1.30%, and Germany’s DAX gained by 1.28%. The UK’s FTSE 100 Index ascended by 0.96%. In the STOXX Europe 600 Index, bank stocks once more resumed their sharp decline by the week’s end on unabated concerns surrounding the financial sector. The continued drop reversed any gains made earlier on news that the UBS Group agreed to buy Credit Suisse in a deal brokered by the Swiss authorities. Although there were no specific pronouncements, the focus of investors appeared to have transferred to worries surrounding banks with exposure to commercial real estate.

Japan’s stock markets realized mixed returns for the week. The Nikkei 225 Index gained by 0.19% but the broader TOPIX declined by 0.21%. After the worries created by the developments in the global banking sector over the last weeks. Investor concerns somewhat as the Bank of Japan (BoJ) and four other major central banks announced on March 19 that they were coordinating action to provide liquidity and to ease strains in the global funding markets. The yen gained strength after the U.S. Federal Reserve raised interest rates as expected, but stated that a pause on further hikes is being considered. The yen finished the week at around JPY 130.6 from about $131.8 against the U.S. dollar the week earlier. The yield on the 10-year Japanese government bond remained broadly unchanged at 0.29%. Although Japan’s inflation remains high, price pressures are beginning to ease.

Chinese stock markets gained ground on optimism that the People’s Bank of China (PBOC) will continue to maintain accommodative monetary policies during the current global banking crisis. The Shanghai Stock Exchange Index advanced by 0.46% and the blue-chip CSI 300 gained by 1.72% in local currency terms. Hong Kong’s benchmark Hang Seng Index rose by 2.03%. The PBOC left its benchmark one-year and five-year loan prime rates (LPR) at 3.65% and 4.3%, respectively, for the seventh straight month. The LPRs are based on the interest rates that 18 banks offer their best customers and are published monthly by the PBOC. They are quoted as a spread over the rate on the central bank’s one-year policy loans, known as the medium-term lending facility (MLF). The stance was largely expected after the PBOC left its MLF unchanged the previous week and unexpectedly announced a 25-basis-point cut in the reserve requirement ratio for most banks, suggesting the easing of measures to support the economy.

The Week Ahead

Among the important economic data scheduled for release this week are personal consumption, consumer confidence, and consumer sentiment.

Key Topics to Watch

- Fed Gov. Jefferson speaks

- Advanced U.S. trade balance in goods

- Advanced retail inventories

- Advanced wholesale inventories

- S&P Case-Shiller home price index (20 cities)

- FHFA home price index

- S. consumer confidence

- Fed Gov. Barr testifies to Senate on banks

- Pending U.S. home sales

- Fed Gov. Barr testifies to House on banks

- GDP (2nd revision)

- Initial jobless claims

- Continuing jobless claims

- Boston Fed President Collins speaks

- Personal income (nominal)

- Personal spending (nominal)

- PCE index

- Core PCE index

- PCE (year-over-year)

- Core PCE (year-over-year)

- Chicago Business Barometer

- Consumer sentiment (final)

- Fed Gov. Waller speaks

- New York Fed President Williams speaks

- Fed Gov. Cook speaks

Markets Index Wrap Up