As Wednesday’s data continued to point to a resilient U.S. economy, strategists at JPMorgan Chase & Co. issued a warning about what could be “meaningful” downside risks in the equity market.

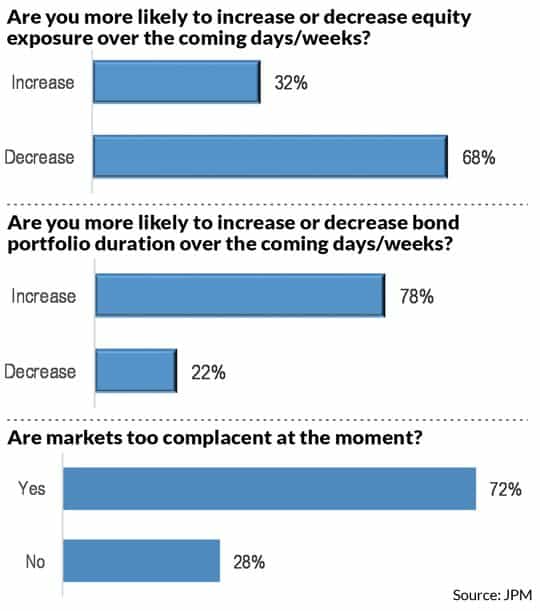

Early results from a survey of JPMorgan’s clients this week showed that 68% were more likely to decrease their exposure to stocks in the coming days and weeks, while 32% were likely to increase it. In addition, 78% said they were more likely to boost bond-portfolio duration over the same period and 22% were likely to decrease it.

The JPMorgan survey is the latest indication that investors may be finally coming around to the view that the Federal Reserve won’t likely pivot toward a rate cut later this year, given the economy’s unexpected strength even after eight straight rate hikes since last March.

Seventy-two percent of respondents in JPMorgan’s survey described markets as being too complacent. January’s stock action had been driven by a “fear-of-missing-out” rally and, for a time, it seemed retail participation was on its way back, with recent sentiment among individual investors turning bullish. Data from Refinitiv Lipper, however, shows investors have been walking away from stock-market funds and going into bonds for weeks.

Wednesday’s economic data included a surprisingly strong 3% jump in retail sales for January, giving fresh hope to the idea that the U.S. can avoid a recession in the first quarter in what some are calling a “no landing” scenario. The report comes a day after January’s consumer-price index underscored that inflation is grudgingly slowing and still sticky, and almost two weeks after a blowout jobs report showed 517,000 new jobs created last month.

Interestingly, U.S. economic strength appears to be translating into greater risks in the financial market, by ensuring the Fed’s rate-hike campaign endures. Indeed, some economists have argued that a “no landing” scenario could sink stocks as a hot labor market and other factors force the Fed to drive rates higher than policy makers and investors currently expect.

On Tuesday, January’s hotter-than-expected CPI report had traders lifting the likelihood of a June rate hike to almost 52%, up from 35% a week ago, and was already raising the possibility that it could deal a massive blow to the stock market. After Wednesday’s retail-sales report, traders were slightly boosting the chances of a half-percentage-point rate hike in March, which would take the fed-funds rate target to between 5% and 5.25%, though the overwhelming likelihood remained in place for a smaller, quarter-point move.

In an email to MarketWatch on Wednesday, Thomas Salopek, JPMorgan’s head of cross asset strategy, said the “upside surprise in the retail sales number is similar to the recent strong jobs print, in that it raises the risk for more restrictive rates, or for restrictive rates to be maintained for longer, a scenario our economists call ‘boiling the frog.’ The impact is reflected well in both U.S. yield and dollar moves, but we remain bearish on equities for Q1, as they have shrugged off the message of the recent data.”

“Boiling the frog” is a metaphor used to describe an unwillingness or inability to perceive gathering threats, even while the temperature is rising. The phrase was also used by analysts at Société Générale in 2017 to describe complacent investors in the role of the frog, which ends up jumping out of boiling water just in time.

Salopek was one of the JPMorgan strategists who wrote in an updated note on Wednesday that “with equities trading near last summer’s highs and at above-average multiples, despite weakening earnings and the recent sharp move higher in interest rates, we maintain that markets are overpricing recent good news on inflation and are complacent of risks. Equity markets appeared to read this month’s central bank meetings as dovish, while dismissing the weak Q4 earnings and the implications of the strong U.S. payroll report for both monetary policy and corporate margins.”

“We see the equity risk/reward as skewed to the downside, as upside potential for markets is likely fairly limited given stretched valuations and high rates, while downside could be meaningful, e.g. in case of a further weakening of activity, persisting inflation, higher terminal rates, or a resurgence of geopolitical risk,” the strategists said.

Other preliminary results of the survey that 38% percent of respondents see the next U.S. recession starting in the first half of 2024, while 34% expect the downturn to begin in the second half of this year.

On Wednesday, all three major U.S. stock indexes DJIA, +0.11% SPX, +0.28% finished higher even after the retail-sales report pointed to the potential for more restrictive interest rates. Meanwhile, the 10-year Treasury yield TMUBMUSD10Y, 3.784% finished the New York session at its highest level of the year, 3.806%.