Stock Markets

Stocks ended sharply lower for the second consecutive week on fears that the economy will experience a hard landing due to the Federal Reserve’s most aggressive rate hike since 1994. The week began with a sell-off that left every stock in the S&P 500 down at one point, a phenomenon that has not happened since 1996. Analysts attributed this to continuing inflation worries that were sparked the preceding Friday by a surprise increase in the May consumer inflation data. It was further worsened by a report on Monday by the Wall Street Journal that Fed officials were mulling an increase in interest rates by 75 basis points (or 0.75%) on the coming Wednesday meeting, something the market priced in the week earlier as having only a 2% chance of happening.

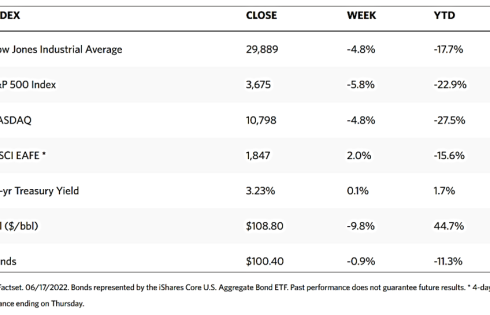

The Dow Jones Industrial Average (DJIA) lost 4.79% for the week while the S&P 500 came down by 5.79%. The Nasdaq composite also dropped 5.79%. The NYSE composite fell by 6.62%. Many investors are concerned that a recession is likely if businesses succumb to high-interest rates and a possible credit crunch. The S&P 500 underwent its worst weekly decline since March 2020 and officially entered a bear market as it closed the week almost 24% below its highest level in January. The percentage of S&P 500 stocks that were trading above their 50-day moving average plunged below 5% for the past week. This is the lowest level since the pandemic began in 2020.

U.S. Economy

Headline inflation remains unrelentingly high due to geopolitical shocks to oil and food prices as well as persistent bottlenecks in the supply chain. This has forced the Fed to further accelerate its rate-hiking strategy in an intensified effort to mitigate inflation expectations, increasing the risks of a Federal-induced recession. According to several reports, there is a possibility that Fed tightening and the surge in mortgage rates will have an impact on the housing sector. In May, building permits fell 7% to their lowest limit since September 2021. Housing starts dropped 14.4%, the biggest since the pandemic began. Weekly jobless claims were 229,000, higher than the expected 210,000.

Furthermore, there was a surprise contraction in Mid-Atlantic factory activity, the first since May 2020, mirroring a contraction and weaker-than-expected reading in the New York region that was reported earlier in the week. Overall retail sales fell 0.3% in May due to a sharp decline in auto purchases that reflected, in part, the higher rates on car loans. Even with the exclusion of autos, sales rose only 0.5% which was lower than the consensus expectation of 0.8%. Sales rose only 0.1% excluding gasoline. The data confirms that consumers were buying less in real terms in light of the higher year-over-year increase in consumer inflation (8.6%) than in non-inflation-adjusted retail sales (8.1%). By these indications, fears of an impending recession are materializing.

Metals and Mining

The gold market is expected to absorb a 2% loss for the week, although many investors in precious metals see the price movement as a positive development with gold standing up to the most aggressive Federal Reserve actions in almost three decades. With inflation at a fresh 40-year high last month, the Fed had no option but to raise interest rates by 75 basis points during the week. Simultaneously, the central bank also took further aggressive action since it anticipates that interest rates may potentially increase to 3.5% by the end of 2022 and possibly hit 4.0% in 2023. Markets are pricing in an additional 75 basis point increase next month as Federal Reserve Chair Powell proclaimed that inflation remains the biggest economic threat. Despite these concerns, gold prices maintain their ground just slightly below $1,850 per ounce. This is a psychological support level for investors during the past month. While gold prices ended negative week-on-week, by comparison, they still outperform equities.

Gold closed the week prior at $1,871.60 and ended this week at $1,839.39 per troy ounce, a small contraction of 1.72%. Silver also fell marginally by 1.01%, from the previous week’s close of $21.89 to last week’s close of $21.67 per troy ounce. Platinum edged from $977.50 one week earlier to $933.98 per troy ounce this week for a drop of 4.45%. Palladium began the week’s trading at $1,934.12 and ended at $1,818.61 per troy ounce for a 5.97% decline. The 3-mo trading prices of base metals tracked the same direction as precious metals. Copper ended the previous week at $9,615.00 and this week at $8,961.50 per metric tonne, a dive of 6.80%. Zinc began at $3,762.00 and closed the week at $3,523.50 per metric tonne for a price depreciation of 34%. Aluminum fell 9.53% from the earlier week’s close at $2,761.00 to this week’s close at $2,498.00 per metric tonne. Tin lost 15.12% week-on-week, from its previous close at $36,740.00 to this week’s close at $31,184.00 per metric tonne.

Energy and Oil

Due to the adoption of sanctions by the European Union, Russia appears to embark on retaliation by holding back its natural gas exports. There have been large reductions in Russian gas flows to Europe throughout this past week, with Germany, Italy, and France receiving less than half of their usual volumes. The Russian majority state-owned multinational energy company Gazprom blames the sanctions that hinder maintenance, while the European countries perceive the unexpected declines as a sign that the Kremlin is trying to get even for past sanctions by limiting the supply of gas. As a result, it is not only oil and oil products that are trading well above historical averages, but also natural gas. Oil prices fell on Friday morning due to heightened fears of an impending recession. In the U.S., the Biden Administration is looking into possibly capping fuel exports out of the U.S. as gasoline outflows rise to 750,000 barrels per day this year. This matter will likely be raised next week at a meeting between Energy Secretary Granholm and oil refiners. In the meantime, the OPEC+ admits its underproduction of oil, below its target in May by 2,695 barrels per day, and bringing total levels of deal compliance to 256%. Several African producers are stuck in force majeure events and Russian production declined in retaliation for sanctions against it.

Natural Gas

At all major locations this report week (June 8 to June 15, 2022), natural gas spot prices fell. The Henry Hub price dropped from $9.46 per million British thermal units (MMBtu) at the start of the week, to $7.72/MMBtu at the end of the week. International natural gas spot prices were mixed for the week. The weekly average swap prices for liquefied natural gas (LNG) cargoes in East Asia fell $0.68 to a weekly average of $23.09/MMBtu. At the Title Transfer Facility in the Netherlands, Europe’s most liquid natural gas spot market, the day-ahead spot price rose $3.21 to a weekly average of $27.70/MMBtu. Last year, during the same week (ending June 16, 2021), the price in East Asia was $10.92/MMBtu and at the TTF it was $10.01/MMBtu.

In the U.S. market, prices along the Gulf Coast dropped as the Freeport LNG outage was expected to last three months or more. Prices in the Midwest fell with the national average. In the meantime, prices across the West declined with the national average, even as temperatures resulted in increased demand for air conditioning across the Southwest. Prices in the Northeast fell from the high levels of a week ago. U.S. natural gas supply increased week-over-week, as higher net imports from Canada help to meet Midwest demand. U.S. natural gas demand increased as temperatures exceeded normal levels across much of the country. U.S. LNG exports decreased by one vessel this week from last week.

World Markets

European shares fell sharply on worries that economic growth may slow down after several banks announced rate increases. The pan-European STOXX Europe 600 Index ended the week 4.60% lower. Major indexes substantially declined, with France’s CAC 40 Index losing 4.92%, Germany’s DAX Index sliding 4.62%, and Italy’s FTSE MIB Index pulling back by 3.36%. the UK’s FTSE 100 Index lost 4.12% of its value. Fears of another eurozone debt crisis were stoked after a jump in borrowing costs for some heavily indebted member states, prompting an unscheduled meeting of the European Central Bank’s (ECB) Governing Council. After the ad hoc meeting, the ECB released a statement that it would take action to stem the widening yield spread between member states’ sovereign bonds. Such measures would include targeted adjustments in reinvesting the proceeds from maturing debt in the portfolio associated with the central bank’s emergency purchase program. Furthermore, the ECB will seek to develop a new tool to help ease the “fragmentation” in borrowing costs.

In Japan, the stock markets took a sharp dive last week. The Nikkei lost 6.69% and the broader TOPIX index dropped 5.52%. the U.S. Federal Reserve’s announcement of its steepest interest rate hike since 1994 sparked fears of a recession, coincidental with the move by other central banks to curb the surging inflation. The Bank of Japan (BoJ), contrary to the rest of the central banks, maintained its ultralow interest rates, The yield on the 10-year Japanese government bond (JGB) dipped slightly to 0.24% from 0.25% at the end of the week before. It breached the top of the BoJ’s 0.25% policy bank briefly early in the week, causing the central bank to announce an additional, unscheduled outright purchase of JGBs. The yen continued to hover around a 24-year low but it gained some strength over the week, treading at approximately JPY 134.3 against the U.S. dollar, from the earlier week’s JPY 134.4.

Contrary to the rest of the bourses in the West, China’s stock markets advanced with the anticipation that a pickup in fixed asset investments would put the economy back on track. The broad, capitalization-weighted Shanghai Composite Index gained 1.0% and the blue-chip CSI 300 Index, which keeps track of the largest-listed companies in Shanghai and Shenzhen, rose 1.4%, attaining its highest level in three months. The country’s state planner approved 10 fixed asset investments worth CNY 121 billion (USD 18.1 billion) in May, more than six times that of April. The jump in investor sentiment was also impacted by data showing the unexpected growth in May’s industrial production, and from hopes of increased policy support following weak housing market data. Relaxed coronavirus measures in Beijing further improved market sentiment. The yuan remained flat against the U.S. dollar and ended at 6.70 from 6.69 the week before.

The Week Ahead

In the coming week, expect important economic data to be released including the Markit PMI services composite and the Michigan consumer sentiment survey. Several Fed officials are scheduled to speak to give their take on the direction of monetary policy and the economy.

Key Topics to Watch

- Louis Fed President James Bullard speaks

- Chicago Fed national activity index

- Existing home sales (SAAR)

- Cleveland Fed President Loretta Mester speaks

- Richmond Fed President Tom Barkin speaks

- Fed Chair Jerome Powell testifies on monetary policy at Senate Banking Committee

- Chicago Fed President James Bullard speaks

- Initial jobless claims

- Continuing jobless claims

- Current account deficit

- S&P Global U.S. manufacturing PMI (flash)

- S&P Global U.S. services PMI (flash)

- Fed Chair Jerome Powell testifies on monetary policy at House Financial Services Committee

- Louis Fed President James Bullard speaks

- UMich consumer sentiment index (final)

- 5-year inflation expectations (final)

- New home sales (SAAR)

- San Francisco Fed President Mary Daly speaks

Markets Index Wrap Up