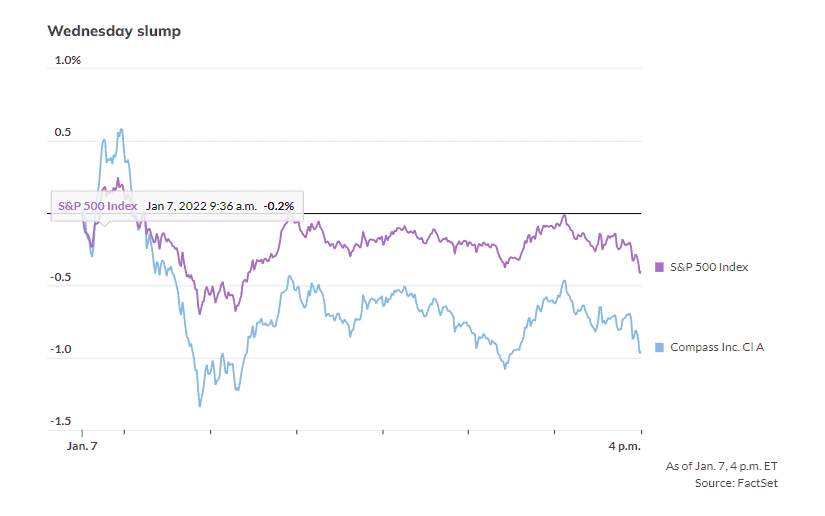

The stock market saw its decline deepen Wednesday afternoon after the release of minutes from the Federal Reserve’s mid-December meeting pointed to a more aggressive plan of policy tightening than market participants had been anticipating for 2022.

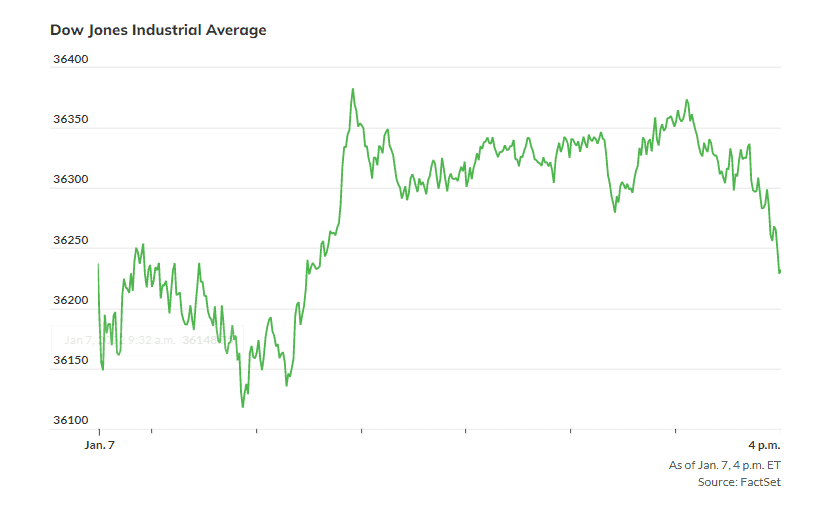

At last check, the Dow Jones Industrial Average DJIA, -0.01% had pivoted from a modest gain to a solid loss, down 230 points, or 0.6%, at 36,571, all but dashing hopes that the blue-chip index would produce a third consecutive record closing to start a calendar year, something that it hasn’t done since 1959.

Minutes revealed robust talk among some Fed officials around the central bank potentially moving to raise rates and also cut its current $8.8 trillion sized balance sheet sooner than expected to help tackle higher costs of living.

Meanwhile, the yield on the 10-year Treasury note TMUBMUSD10Y, 1.767% rose to around 1.70% after the Fed’s minutes were distributed.

Here’s what some strategists and analysts were saying about the account of the meeting and how it alters (or doesn’t) the policy trajectory for the markets in 2022:

“Important to minutes discussion will be the extent of QT — quantitative tightening. When will Fed begin to unwind balance sheet by allowing maturing securities to run off?” wrote John Lynch, chief investment officer at Comerica Wealth Management, in an emailed statement. “This will prove important, as it is a more subtle form of policy tightening,” he wrote.

Meanwhile, Chris Zaccarelli, chief investment officer for Independent Advisor Alliance, said the minutes indicate how important the Fed views normalizing its policy amid surging inflation.

“Given the twin concerns of rising inflation and potential for negative growth surprises, you can see why they have urgency in completing their tapering as soon as possible, while still leaving optionality for the timing of the first rate hike,” he wrote.

The IAA CIO said that he believes the Fed will move quicker and sooner on policy tightening but noted that one difficult question remains unanswered.

“What is harder to forecast is to what level of market selloff they are willing to tolerate before changing course — is it 15%? or 20% ? — we believe the Fed will endure some short term volatility in the stock market in order to remove all of the monetary accommodation they’ve injected into markets, however, they are still likely to heed warnings of recession from the stock market (e.g. a drop of close to 20%) and would pause their activities in that event,” wrote Zaccarelli.

Market-based projections had priced in about three interest-rate hikes in 2022 from the current levels that range between 0% and 0.25%.

Cliff Hodge, chief investment officer for Cornerstone Wealth, on Wednesday wrote that the fact that the FOMC participants are “discussing faster and more aggressive rate hikes, alongside a faster pace of balance sheet normalization [aka quantitative tightening or QT) than the last hiking period, indicate that the Fed “put” for the stock market has been repriced lower.

In markets, a put is an option that gives the holder the right but not the obligation to sell the underlying instrument at a set price by a certain time—a valuable hedge if a bullish position goes south. The Fed put is a reference to the idea that the central bank would take steps to soothe markets in the event of a violent downturn.

Ian Shepherdson, chief economist at Pantheon Macroeconomics suggested that the market may be overreacting to the minutes and that the Fed may not so eager to shrink its balance sheet.

“We expect much more on this question at upcoming meetings, but we remain of the view that the Fed is unlikely to dive into outright balance sheet contraction in a hurry,” Shepherdson wrote.

“Rate increases send a clearer message to the public, and we see no pressing need to take the risks [associated] with shrinking the balance sheet if the inflation numbers head down in the way we expect in the spring,” the economist wrote.