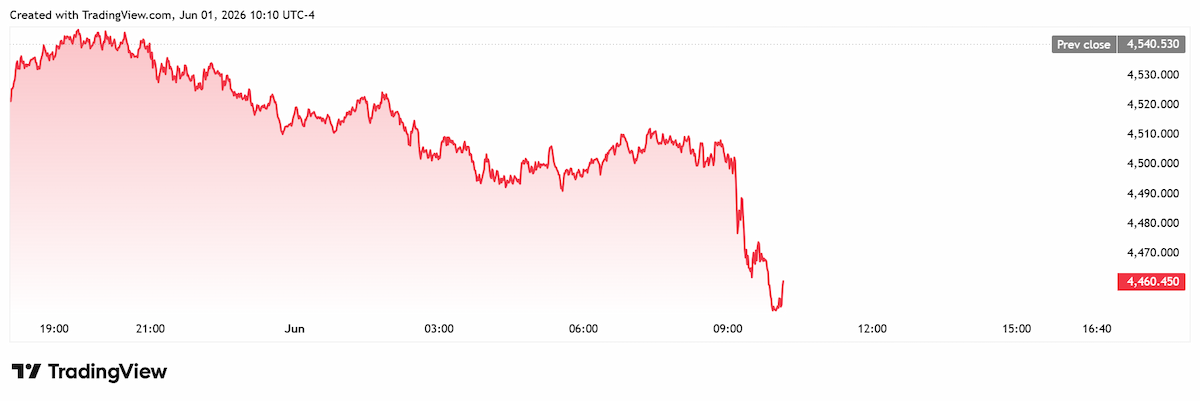

Gold is trading near session lows after the latest data showed the U.S. manufacturing sector beating expectations last month, with prices also moderating in May.

The Institute for Supply Management (ISM) announced on Monday that its Manufacturing Purchasing Managers Index rose to 54 in May, its highest reading since May 2022, after posting a 52.7 reading in April. The headline number was higher than expected, as consensus forecasts looked for a reading of 53.

“In May, U.S. manufacturing activity remained in expansion territory, growing at a faster pace compared to the month before,” said Susan Spence, Chair of the ISM Manufacturing Business Survey Committee. “Of the five subindexes that make up the PMI, the New Orders index indicated faster growth compared to the previous month, the Supplier Deliveries index stayed the same, the Production Index grew at a faster rate, and the Employment and Inventories indexes remained in contraction, though both improved.”

Spot gold fell to a session low of $4,447.86 around 10 a.m. ET, and last traded at $4,460.05 per ounce for a loss of 1.77% on the day.

The components of the report showed an improving picture in key areas, with New Orders, Production and Employment improving from April while Prices moderated.

“The New Orders Index expanded for the fifth consecutive month after four straight readings in contraction, registering 56.8 percent, up 2.7 percentage points compared to April’s figure of 54.1 percent,” Spence noted. “The May reading of the Production Index (54.3 percent) is 0.9 percentage point higher than April’s reading of 53.4 percent. The Prices Index remained in expansion (or ‘increasing’ territory), registering 82.1 percent, a 2.5-percentage point decrease from April’s reading of 84.6 percent. The Backlog of Orders Index registered 52.2 percent, up 0.8 percentage point compared to the 51.4 percent recorded in April. The Employment Index registered 48.6 percent, up 2.2 percentage points from April’s figure of 46.4 percent.”

Bill Adams, Chief U.S. Economist at Fifth Third Commercial Bank, told Kitco News that a number of crosswinds are buffeting the U.S. economy this year.

“Of course the Iran War, but also the AI boom, the fiscal stimulus package passed last year, and the Fed’s rate cuts passed in late 2025,” he said. “The net effect of these crosswinds is an economy that continues to grow at a good clip, but with quite uneven distribution across sectors.”

Adams said manufacturing is actually a beneficiary of these crosswinds. “Defense, aerospace, and semiconductors are part of this,” t\he noted. “But so is capital equipment demand, boosted by the bonus depreciation clause of last year’s tax and spending bill. Also, the backlog of business decisions delayed in 2025 because of tariff uncertainty looks like it is starting to flow through to purchases and production. To the downside, the relative weakness of construction is a big headwind to demand for construction materials.”

“For the overall economic outlook, the ISM survey shows that the economy continues to expand in the second quarter, albeit with winners and losers,” he said. “The economy looks to have grown at a decent clip in the first half of 2026. The slowdown in the first quarter was largely a function of weak additions to business inventories, a drag which should swing to a tailwind in coming quarters.

“If the Strait of Hormuz opens in the next days to weeks (as is currently priced into financial markets) and ends the disruption to global energy supplies, the U.S. economy can realize another year of respectable economic growth in 2026.”