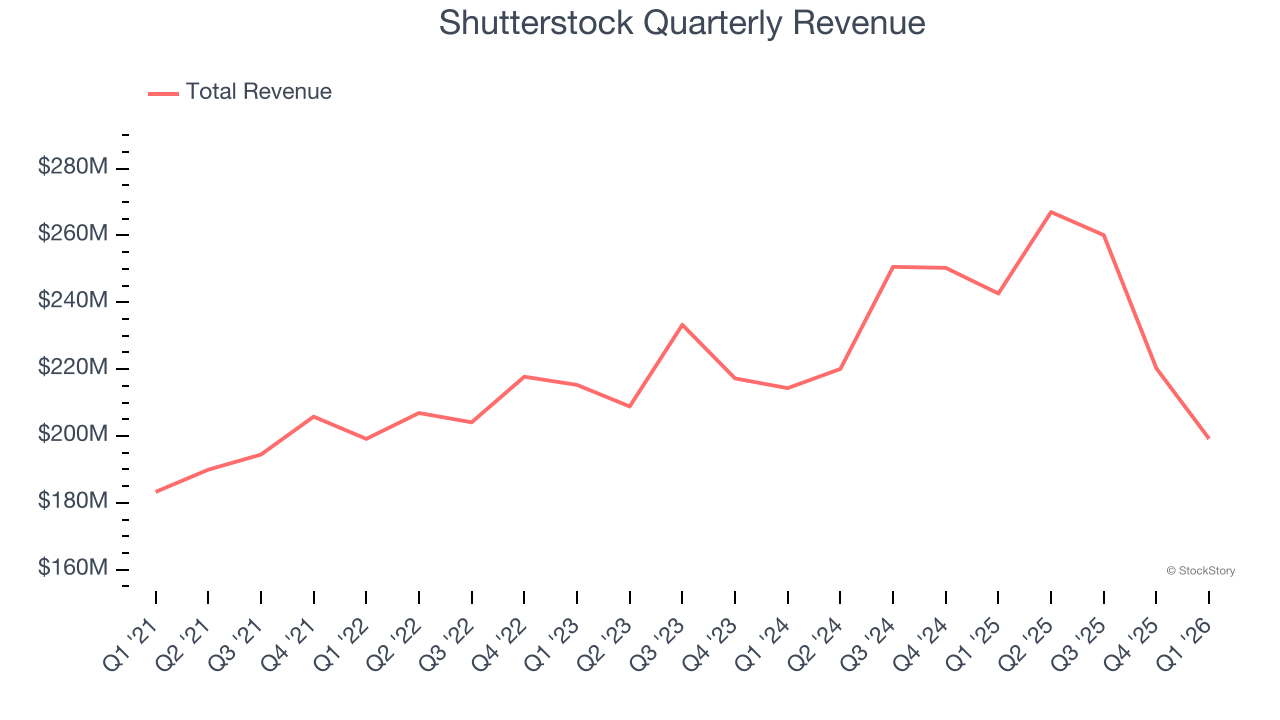

Stock photography and footage provider Shutterstock (NYSE:SSTK) missed Wall Street’s revenue expectations in Q1 CY2026, with sales falling 17.9% year on year to $199.2 million. Its non-GAAP profit of $0.58 per share was 39.6% below analysts’ consensus estimates.

Commenting on the Company’s performance, Paul Hennessy, the Company’s Chief Executive Officer, said, “During the first quarter, we maintained a strong focus on operational discipline and cost management, delivering $43 million in Adjusted EBITDA in the face of ongoing industry headwinds. While first quarter revenue was impacted by a slower start in our Content business than expected and the timing of revenue recognition associated with data licensing deals, we continue to invest in areas that will drive long-term growth and remain committed to simplifying our product offerings to better meet our customers’ needs.”

Company Overview

Originally featuring a library that included many of founder Jon Oringer’s photos, Shutterstock (NYSE:SSTK) is now a digital platform where customers can license and use hundreds of millions of pieces of content.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Shutterstock’s sales grew at a sluggish 3.9% compounded annual growth rate over the last three years. This was below our standard for the consumer internet sector and is a rough starting point for our analysis.

This quarter, Shutterstock missed Wall Street’s estimates and reported a rather uninspiring 17.9% year-on-year revenue decline, generating $199.2 million of revenue.

Looking ahead, sell-side analysts expect revenue to decline by 4.3% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar.

Cash Is King

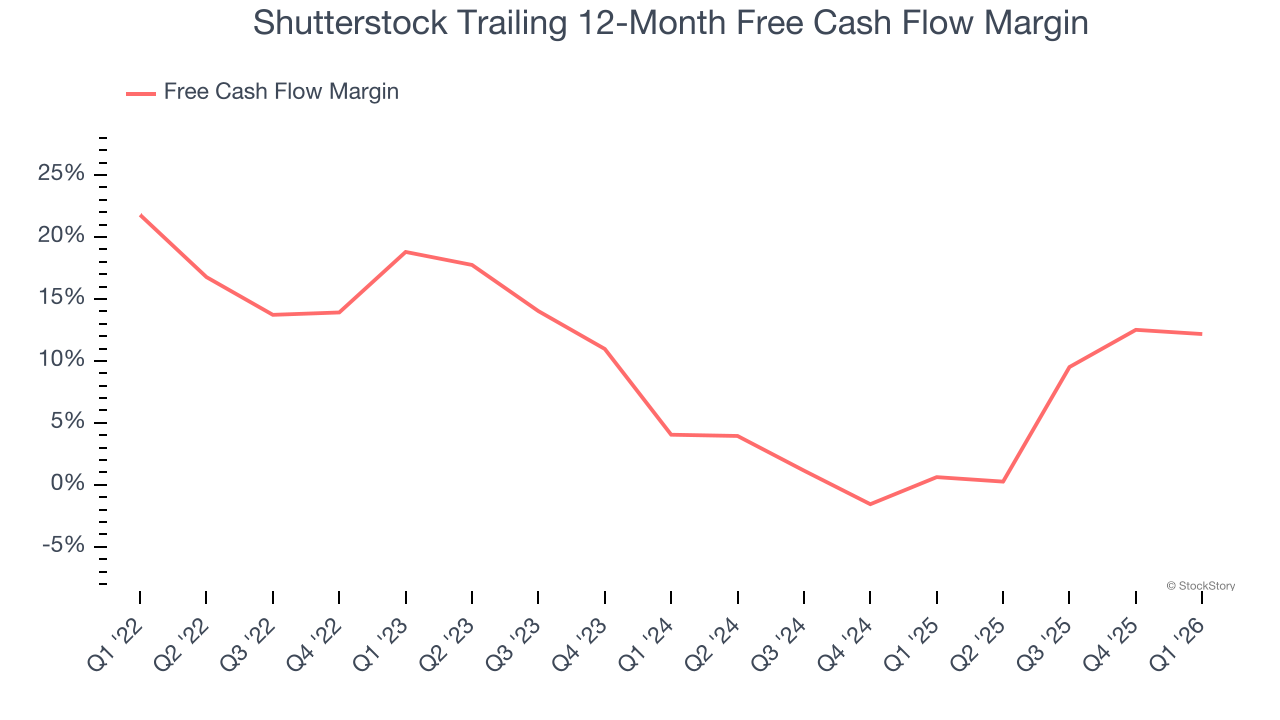

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Shutterstock has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.3% over the last two years, slightly better than the broader consumer internet sector.

Taking a step back, we can see that Shutterstock’s margin dropped by 6.6 percentage points over the last few years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal increasing investment needs and capital intensity.

Shutterstock’s free cash flow clocked in at $5.78 million in Q1, equivalent to a 2.9% margin. The company’s cash profitability regressed as it was 3.1 percentage points lower than in the same quarter last year, suggesting its historical struggles have dragged on.