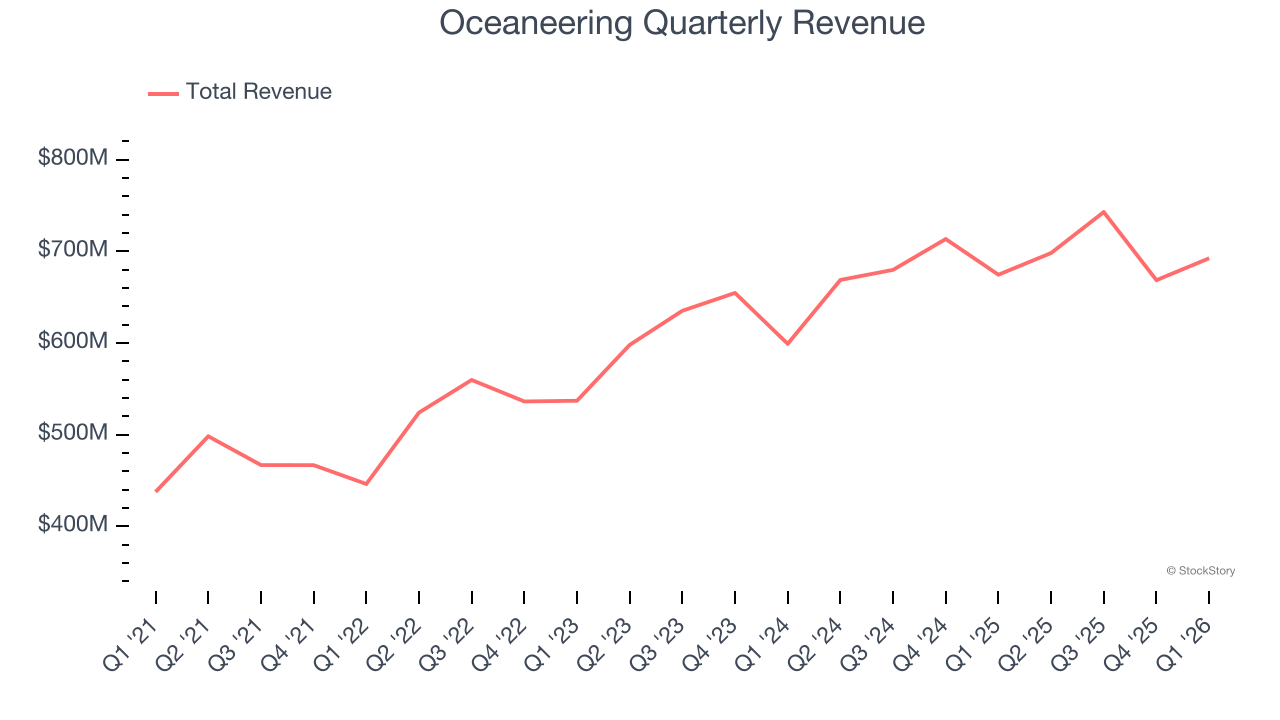

Offshore services provider Oceaneering International (NYSE:OII) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 2.7% year on year to $692.4 million. Its GAAP profit of $0.36 per share was 7.7% below analysts’ consensus estimates.

Company Overview

Deploying a fleet of 250 tethered underwater robots around the globe, Oceaneering International (NYSE:OII) provides remotely operated underwater vehicles and subsea equipment for offshore energy exploration.

Revenue Growth

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Over the last five years, Oceaneering grew its sales at a decent 10.1% compounded annual growth rate. Its growth was slightly above the average energy upstream and integrated energy company and shows its offerings resonate with customers.

Within Energy, a singular timeframe, even if it’s quite long-term, only sheds light on how well a company rode the last commodity cycle. To better assess whether a company compounds through cycles, we validate our view with an even longer, ten-year view. Oceaneering’s recent performance shows its demand has accelerated as its revenue was flat over the last ten years.

This quarter, Oceaneering reported modest year-on-year revenue growth of 2.7% but beat Wall Street’s estimates by 3.5%.

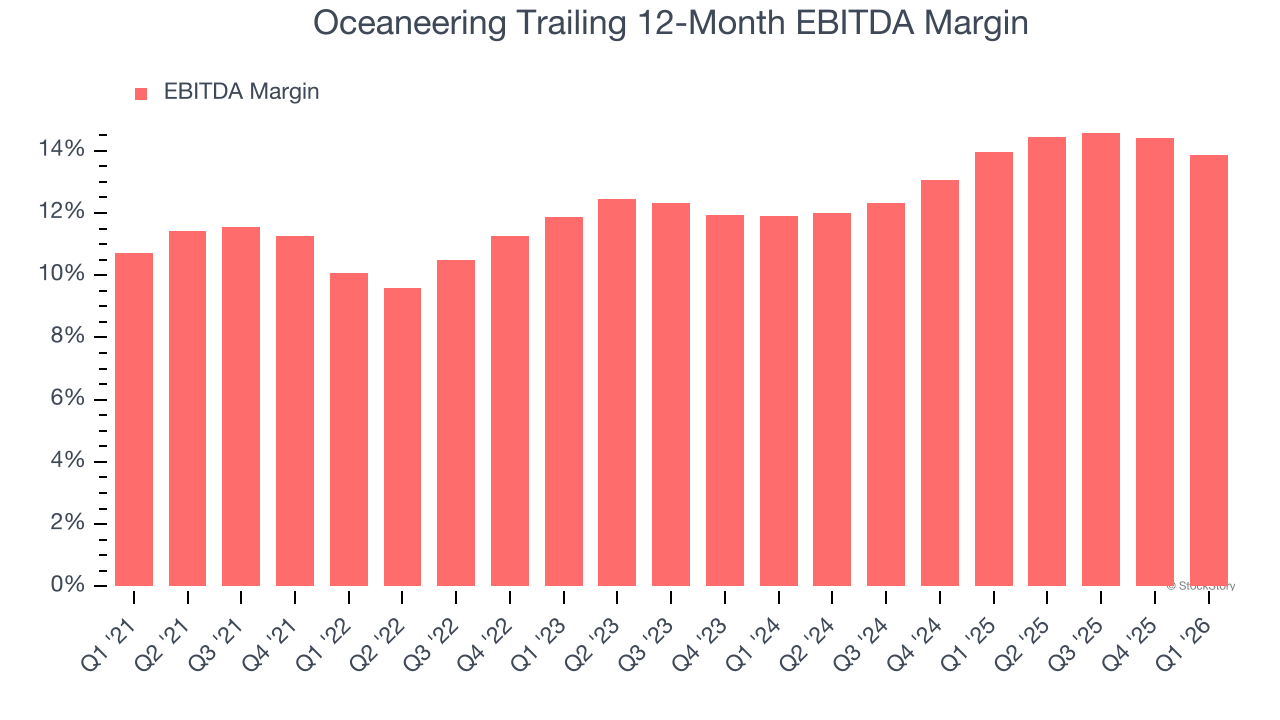

Adjusted EBITDA Margin

Adjusted EBITDA margin is an important measure of profitability for the sector and accounts for the gross margins and operating costs mentioned previously. Unlike operating margin, it is not distorted by accounting conventions around reserves, drilling costs, and assumptions on commodity consumption from the well or basin. Adjusted EBITDA highlights the economic reality of how much cash the rock produces before the capital structure (debt service) and the drilling budget (capex) are considered.

Oceaneering was profitable over the last five years but held back by its large cost base. Its average EBITDA margin of 12.5% was among the worst in the energy upstream and integrated energy sector.

On the plus side, Oceaneering’s EBITDA margin rose by 3.8 percentage points over the last year.

This quarter, Oceaneering generated an EBITDA margin profit margin of 12.1%, down 2.2 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue. This adjusted EBITDA fell short of Wall Street’s estimates.

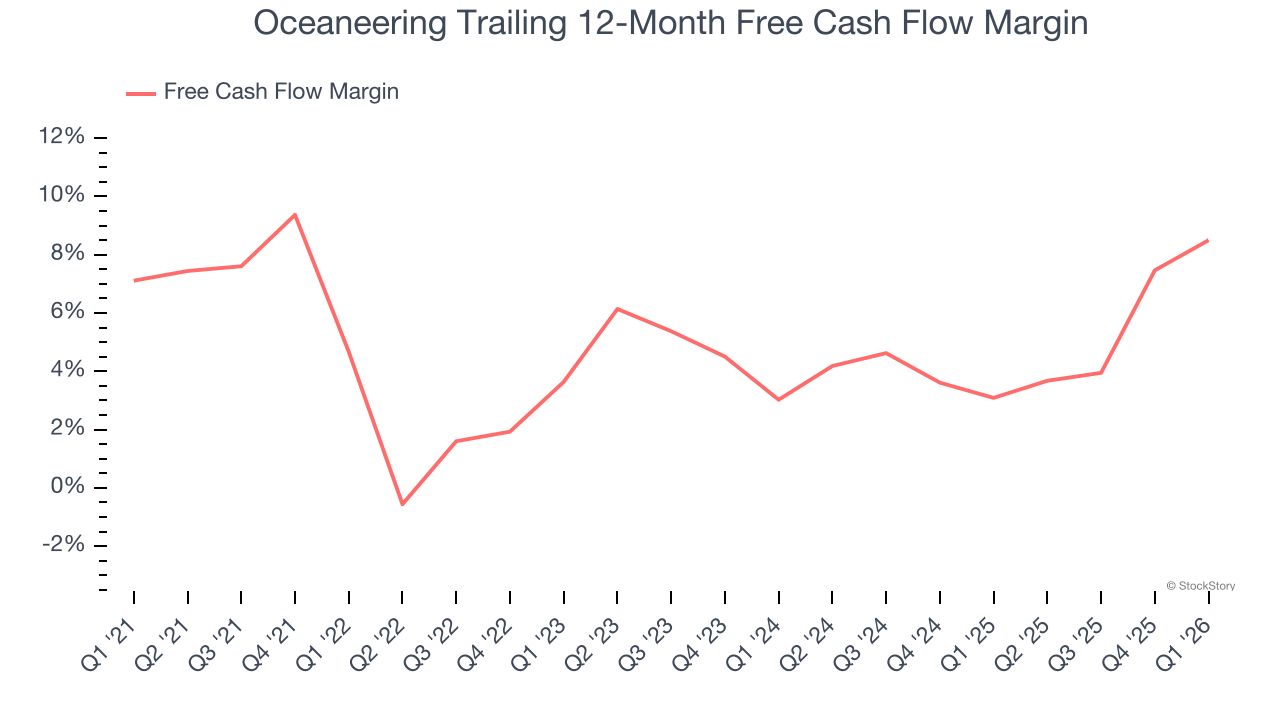

Cash Is King

Adjusted EBITDA shows how profitable a company’s existing “rock” is before financing and reinvestment, while free cash flow shows how much value remains after paying to replace those wells. Because production declines over time, strong EBITDA can coexist with weak FCF if drilling is expensive or declines are steep. FCF therefore captures both operating efficiency and the cost of sustaining production.

Oceaneering has shown weak cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 4.7%, below what we’d expect for an upstream and integrated energy business.

Absolute FCF margin levels matter but so does stability of free cash flow. All else equal, we’d prefer a 25.0% average free cash flow margin that is quite steady no matter how commodity prices behave rather than extremely high margins when times are good and negative ones when they’re tough.

Oceaneering’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 20.6 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of Oceaneering? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Oceaneering burned through $76.52 million of cash in Q1, equivalent to a negative 11.1% margin. The company’s cash burn slowed from $106.8 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.