As inflationary pressures rise and energy costs remain elevated, Asian markets are navigating a complex economic landscape that includes geopolitical uncertainties and fluctuating investor sentiment. In this environment, identifying stocks believed to be trading below their estimated value can offer potential opportunities for investors looking to capitalize on market inefficiencies. A good stock in such conditions often exhibits strong fundamentals and resilience against broader economic challenges, making it an attractive consideration for those seeking value amidst volatility.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

|

Name |

Current Price |

Fair Value (Est) |

Discount (Est) |

|

Yurtec (TSE:1934) |

¥2476.00 |

¥4942.16 |

49.9% |

|

XD (SEHK:2400) |

HK$56.85 |

HK$113.03 |

49.7% |

|

Nanya Technology (TWSE:2408) |

NT$311.50 |

NT$622.38 |

50% |

|

Musashi Seimitsu Industry (TSE:7220) |

¥5440.00 |

¥10846.47 |

49.8% |

|

Moshi Moshi Retail Corporation (SET:MOSHI) |

THB34.75 |

THB69.31 |

49.9% |

|

LianChuang Electronic TechnologyLtd (SZSE:002036) |

CN¥8.38 |

CN¥16.71 |

49.8% |

|

GenFleet Therapeutics (Shanghai) (SEHK:2595) |

HK$35.72 |

HK$70.99 |

49.7% |

|

freee K.K (TSE:4478) |

¥2182.00 |

¥4323.93 |

49.5% |

|

Flat Glass Group (SEHK:6865) |

HK$8.25 |

HK$16.42 |

49.7% |

|

COVER (TSE:5253) |

¥1466.00 |

¥2917.62 |

49.8% |

Let’s review some notable picks from our screened stocks.

Mitsui Chemicals

Overview: Mitsui Chemicals, Inc. operates globally in sectors such as mobility, life and health care, basic and green materials, and ICT, with a market cap of ¥777.05 billion.

Operations: The company’s revenue segments are comprised of ¥285.76 billion from ICT Solutions, ¥264.26 billion from Life & Healthcare Solutions, ¥669.62 billion from Basic & Green Materials (including Urethane), and ¥518.47 billion from Mobility Solutions (including Functional Polymeric Materials).

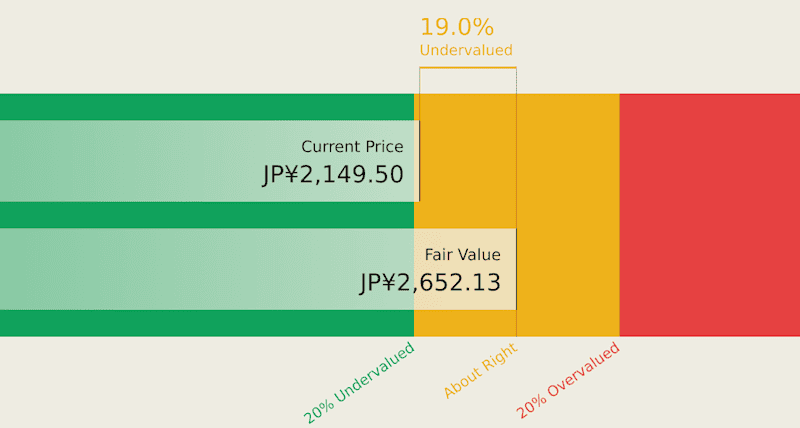

Estimated Discount To Fair Value: 19%

Mitsui Chemicals is trading 19% below its estimated fair value, with earnings forecast to grow significantly at 25.15% per year, outpacing the Japanese market’s growth rate. Despite having a high level of debt and a low projected return on equity (9.3%), the company maintains reliable dividends at 3.49%. Recent buybacks, totaling ¥29.99 billion, reflect management’s confidence in its valuation and potential for future cash flow growth despite slower revenue expansion (4.8%).

Taiheiyo Cement

Overview: Taiheiyo Cement Corporation operates in the cement, mineral resources, environmental, and construction materials sectors both in Japan and internationally, with a market cap of ¥432.24 billion.

Operations: The company’s revenue is primarily derived from its cement segment at ¥667.91 billion, followed by mineral resources at ¥90.86 billion, environmental business at ¥81.78 billion, and construction materials at ¥43.43 billion.

Estimated Discount To Fair Value: 29.9%

Taiheiyo Cement is trading 29.9% below its estimated fair value, with earnings projected to grow significantly at 21.6% annually, surpassing the Japanese market’s growth rate. Despite a lower net profit margin and high debt levels, recent share buybacks totaling ¥9.99 billion signal management’s confidence in enhancing shareholder returns and capital efficiency. However, revenue growth forecasts remain modest at 4.5%, slightly above the market average but below expectations for robust expansion.

Roland

Overview: Roland Corporation is engaged in the development, manufacturing, marketing, import, and export of electronic musical instruments, equipment, and software both in Japan and internationally with a market cap of ¥122.10 billion.

Operations: The company’s revenue segments include electronic musical instruments at ¥93.20 billion, music production equipment at ¥24.50 billion, and software and services at ¥5.30 billion.

Estimated Discount To Fair Value: 24.4%

Roland Corporation is trading 24.4% below its estimated fair value, with a significant projected earnings growth of 22.8% annually, outpacing the Japanese market. However, its profit margins have decreased from last year and the dividend yield of 3.67% is not well covered by earnings. Despite slower revenue growth forecasts at 3.9%, Roland’s strong future cash flow valuation underscores potential undervaluation in the current market context, although recent financial results are impacted by large one-off items.