It’s common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Salesforce (NYSE:CRM). While profit isn’t the sole metric that should be considered when investing, it’s worth recognising businesses that can consistently produce it.

How Fast Is Salesforce Growing Its Earnings Per Share?

In the last three years Salesforce’s earnings per share took off; so much so that it’s a bit disingenuous to use these figures to try and deduce long term estimates. As a result, we’ll zoom in on growth over the last year, instead. It’s good to see that Salesforce’s EPS has grown from US$5.81 to US$7.00 over twelve months. There’s little doubt shareholders would be happy with that 20% gain.

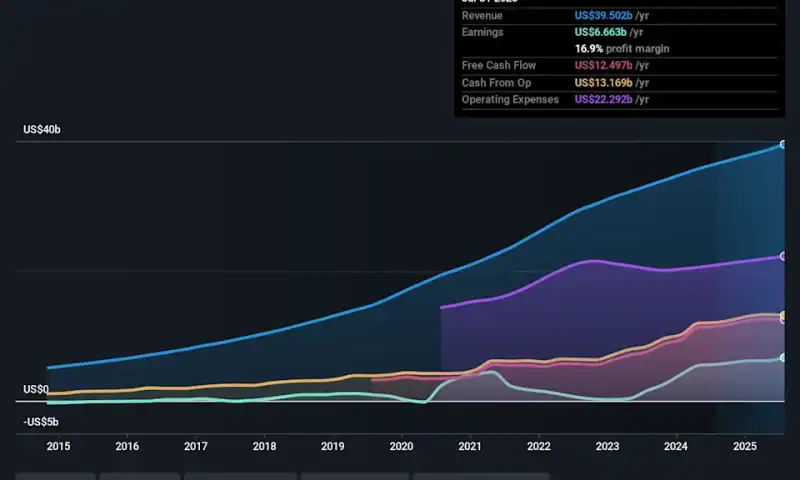

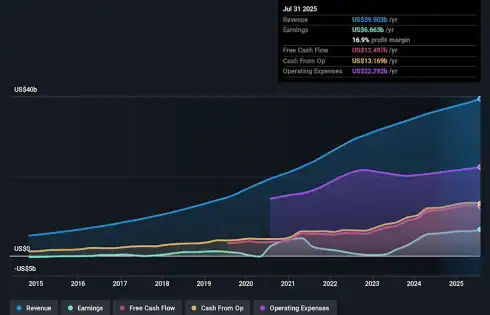

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it’s a great way for a company to maintain a competitive advantage in the market. The music to the ears of Salesforce shareholders is that EBIT margins have grown from 19% to 21% in the last 12 months and revenues are on an upwards trend as well. Both of which are great metrics to check off for potential growth.

You can take a look at the company’s revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

While we live in the present moment, there’s little doubt that the future matters most in the investment decision process. So why not check this interactive chart depicting future EPS estimates, for Salesforce?

Are Salesforce Insiders Aligned With All Shareholders?

We would not expect to see insiders owning a large percentage of a US$235b company like Salesforce. But we are reassured by the fact they have invested in the company. We note that their impressive stake in the company is worth US$6.0b. Investors will appreciate management having this amount of skin in the game as it shows their commitment to the company’s future.

Should You Add Salesforce To Your Watchlist?

One important encouraging feature of Salesforce is that it is growing profits. For those who are looking for a little more than this, the high level of insider ownership enhances our enthusiasm for this growth. The combination definitely favoured by investors so consider keeping the company on a watchlist. Once you’ve identified a business you like, the next step is to consider what you think it’s worth. And right now is your chance to view our exclusive discounted cashflow valuation of Salesforce. You might benefit from giving it a glance today.

Although Salesforce certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see companies with more skin in the game, then check out this handpicked selection of companies that not only boast of strong growth but have strong insider backing.