Xylem (XYL) continues to draw attention after recent share price weakness, with the stock down about 7% over the past month and 13% over the past 3 months, compared with modest 1-year gains.

The recent 30-day share price return of a 6.8% decline and 90-day share price return of a 12.8% decline suggest momentum has cooled, even as the 1-year total shareholder return of 2.9% and 3-year total shareholder return of 26.7% indicate a still positive longer record.

If you are rethinking your exposure to water infrastructure and related technologies, it can be a good moment to broaden your watchlist with a dedicated power grid, technology and infrastructure stock screener such as 27 power grid technology and infrastructure stocks.

With Xylem now trading at $120.44, alongside an indicated 24.0% intrinsic discount and a 31.5% gap to the current analyst price target, you have to ask: is this a genuine entry point, or is the market already baking in future growth?

The recent 30-day share price return of a 6.8% decline and 90-day share price return of a 12.8% decline suggest momentum has cooled, even as the 1-year total shareholder return of 2.9% and 3-year total shareholder return of 26.7% indicate a still positive longer record.

If you are rethinking your exposure to water infrastructure and related technologies, it can be a good moment to broaden your watchlist with a dedicated power grid, technology and infrastructure stock screener such as 27 power grid technology and infrastructure stocks.

With Xylem now trading at $120.44, alongside an indicated 24.0% intrinsic discount and a 31.5% gap to the current analyst price target, you have to ask: is this a genuine entry point, or is the market already baking in future growth?

Most Popular Narrative: 24% Undervalued

With Xylem shares at $120.44 against a narrative fair value of $158.41, the current gap rests on a detailed view of future earnings power and cash flows.

Significant and increasing investment in aging water infrastructure (notably in the U.S. and U.K.) underpins a strong multi year backlog (> $5 billion), with anticipated order rebounds as funding cycles and regulatory timelines normalize, supporting steady revenue growth and greater earnings visibility.

Curious what is baked into that valuation gap? The narrative leans on measured revenue growth, firmer margins, and a premium earnings multiple that still assumes discipline.

Result: Fair Value of $158.41 (UNDERVALUED)

However, you also have to weigh risks such as slower funding cycles in key markets and any slip in execution on acquisitions or large transformation programs that could unsettle expectations.

Another Way To Look At Value

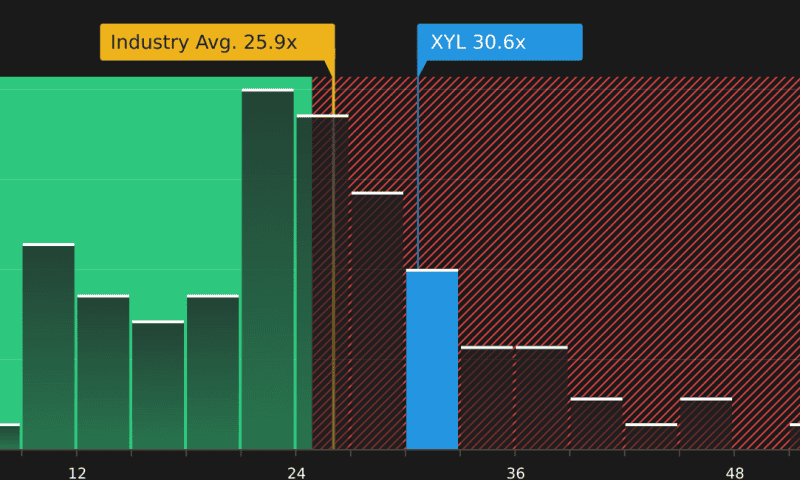

The narrative and DCF work suggest Xylem is 24% undervalued, yet the current 30.6x P/E tells a different story. That is higher than the US Machinery industry at 26.3x, roughly in line with a 30.9x fair ratio and below a 41.4x peer average. Is the discount really that straightforward?