Why Agnico Eagle Mines (AEM) Is On Investors’ Radar Today

Agnico Eagle Mines (NYSE:AEM) has caught investor attention after a period of mixed short term returns, with the stock down about 11% over the past week but up roughly 14% over the past month.

Over the past 3 months, the stock shows a return of about 35%, while the 1 year total return sits near 134%. Those moves are prompting some investors to revisit how the miner’s current share price lines up with its underlying business.

That mix of a 10.9% 7 day share price decline alongside a 31.9% year to date share price return and a very large 3 year total shareholder return suggests momentum has been strong over time, even if short term sentiment has cooled.

If Agnico Eagle Mines has you thinking more broadly about gold exposure, it could be a good moment to scan our list of 28 elite gold producer stocks as potential next ideas to research.

With Agnico Eagle Mines posting a very large 3 year total return and reporting revenue of US$11.91b alongside net income of US$4.46b, you have to ask: is there still value left here, or is the market already pricing in future growth?

Most Popular Narrative: 1% Overvalued

The most followed narrative currently sees Agnico Eagle Mines’ fair value at $221.67, slightly below the last close of $224.75, which sets up a fairly tight valuation debate.

Exploration success and rapid reserve expansion near key long-life assets (notably Detour Lake, Canadian Malartic, and Hope Bay) position Agnico Eagle for significant organic production growth; this supports a long runway of high-quality, low-risk volume expansion that can drive top-line revenue growth and production leverage.

Curious what kind of revenue runway and profit margins are baked into that fair value, and how rich a future earnings multiple the narrative leans on? The full narrative breaks down the growth path, profitability assumptions and discount rate that all have to line up for $221.67 to make sense.

Result: Fair Value of $221.67 (OVERVALUED)

However, that narrative could quickly look stretched if gold prices soften or key projects face delays, cost overruns, or permitting setbacks that hit cash generation.

Another Angle On Valuation

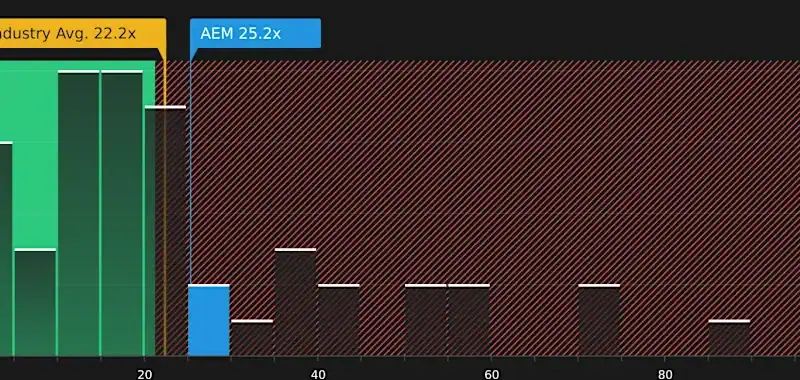

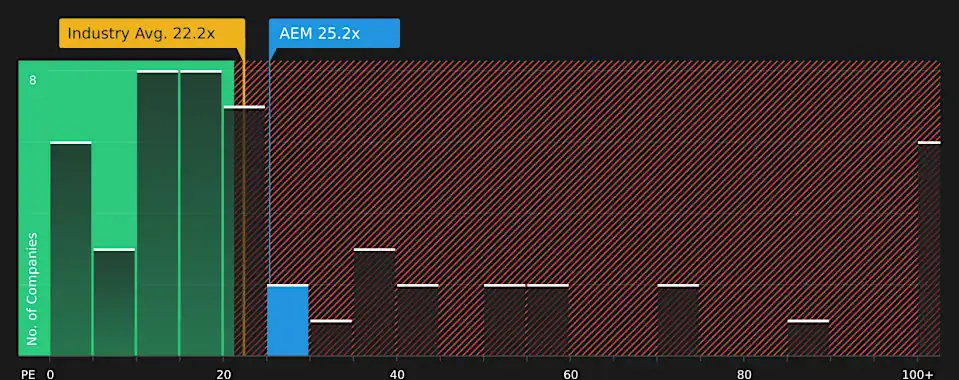

So far, the narrative suggests Agnico Eagle Mines looks about 1% overvalued against a fair value of $221.67. Using a different lens, the current P/E of 25.2x sits below a fair ratio of 27.8x but above the US Metals and Mining average of 22.2x. This points to a premium sector pricing with some valuation cushion. The real question is whether you think that premium is earned or at risk if expectations ease.