Teva Pharmaceutical Industries (NYSE:TEVA) is back in focus after investors reviewed its recent performance metrics, including a past 3 months total return of 25.97% and annual revenue of US$17.26b with net income of US$1.41b.

At a share price of US$33.86, Teva’s short term share price returns over 7 and 30 days have been relatively muted. However, the 90 day share price return of 25.97% and very strong 1 year total shareholder return of 111.62% point to momentum that has built meaningfully over the past year.

If Teva’s rebound has you rethinking where growth could come from next, it may be worth scanning 27 healthcare AI stocks as another way to spot health related opportunities tied to data and automation.

With Teva reporting US$17.26b in revenue, US$1.41b in net income and trading at US$33.86, plus an indicated 42.63% intrinsic discount, is the market offering a genuine entry point or already pricing in future growth?

Most Popular Narrative: 10.8% Undervalued

Teva Pharmaceutical Industries’ most followed valuation story currently anchors fair value at US$37.95 per share versus the last close at US$33.86, framing the stock as trading below that narrative fair value while hinging heavily on future execution in R&D and affordable medicines.

Recent Street research on Teva Pharmaceutical Industries has centered on refreshed price targets, the potential of the R&D pipeline heading into 2026, and the appeal of the affordable medicines theme. Here is how bullish and cautious views are shaping up around valuation, execution, and growth.

Read the complete narrative.

Curious what sits behind that fair value gap and the 2026 focus point? The narrative leans on a specific revenue glide path, firmer profit margins, and a future earnings multiple that assumes investors reward consistent execution rather than just short bursts of progress.

Result: Fair Value of $37.95 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the story could change quickly if reliance on a few branded drugs, pressure on affordable medicines pricing, or a heavy US$15b plus debt load start to bite.

Find out about the key risks to this Teva Pharmaceutical Industries narrative.

Another Angle On Valuation

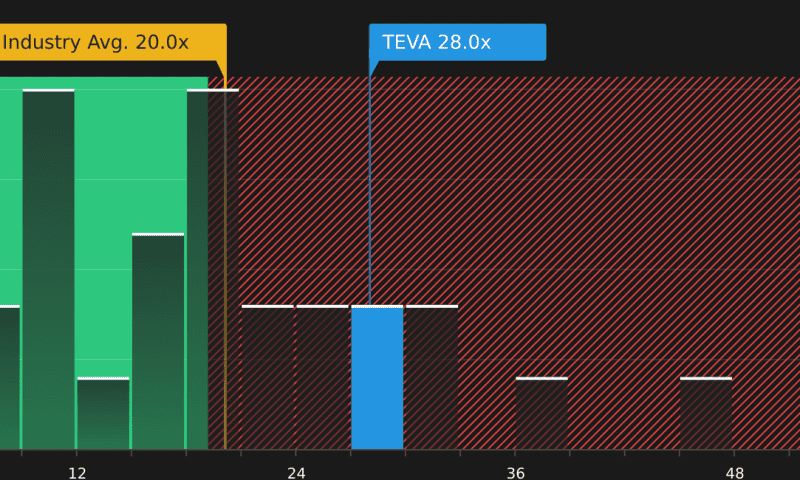

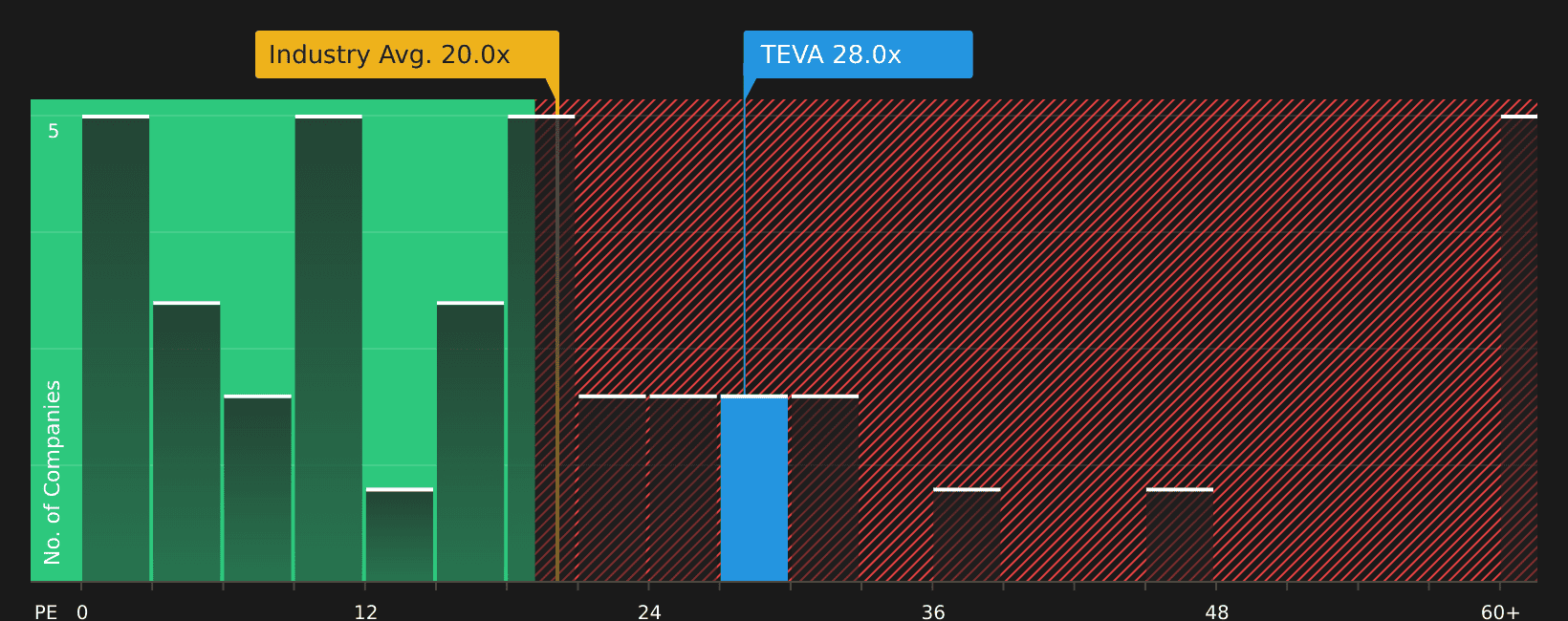

The fair value narrative presents Teva as 10.8% undervalued at US$33.86, but the price tag tells a different story. On a 28x P/E, the shares trade above the US Pharmaceuticals industry at 20x, peers at 21.2x, and the 24.3x fair ratio indicated by our model.

This gap suggests investors are already paying a premium for execution and growth that involve risk. If the market moves closer to the fair ratio, how comfortable are you with the valuation cushion at today’s price?