Hewlett Packard Enterprise stock overview

Hewlett Packard Enterprise (HPE) has drawn investor attention after a strong run over the past month and past 3 months, with returns of 62% and 133% respectively, alongside positive annual revenue and net income growth.

At a latest share price of US$49.20, Hewlett Packard Enterprise has seen strong momentum, with a 30 day share price return of 62% and a year to date share price return of 103.56%. The 1 year total shareholder return of 178.53% and 5 year total shareholder return of 258.31% indicate that investors who stayed invested have seen substantially higher gains than the recent move alone suggests.

If you are looking for other opportunities riding similar technology themes, this is a good moment to scan 48 AI infrastructure stocks

With HPE now at US$49.20 after sharp recent gains, investors are asking a simple question: do the current valuation metrics and growth profile leave any mispricing on the table, or is the market already baking in future growth?

Most Popular Narrative: 64% Overvalued

Hewlett Packard Enterprise’s most followed narrative points to a fair value of about $29.92, well below the latest close at $49.20, which is a wide gap investors will want to understand.

The rapid adoption of AI and machine learning across industries is driving a significant increase in demand for high-performance compute and networking infrastructure, and Juniper’s leading position in data center and AI networking (now part of HPE) is expected to expand HPE’s total addressable market and support multi-year topline revenue growth and margin expansion in higher-value segments. The ongoing acceleration of digital transformation is prompting enterprises to modernize IT architectures with hybrid and multi-cloud deployments, HPE’s growth in hybrid cloud (e.g., GreenLake) and recurring software/services revenue positions it to capture more predictable, higher-margin revenues, improving overall earnings quality and visibility.

Want to see what is sitting behind that valuation gap? The narrative leans on faster earnings growth, richer margins, and a future profit multiple that needs to hold up. Curious which specific revenue and margin paths have been plugged into the model, and how they add up to that fair value.

Result: Fair Value of $29.92 (OVERVALUED)

However, investors still need to factor in risks such as tougher competition in AI infrastructure and networking, as well as the execution challenges around integrating Juniper successfully.

Another View: Cash Flows Tell a Different Story

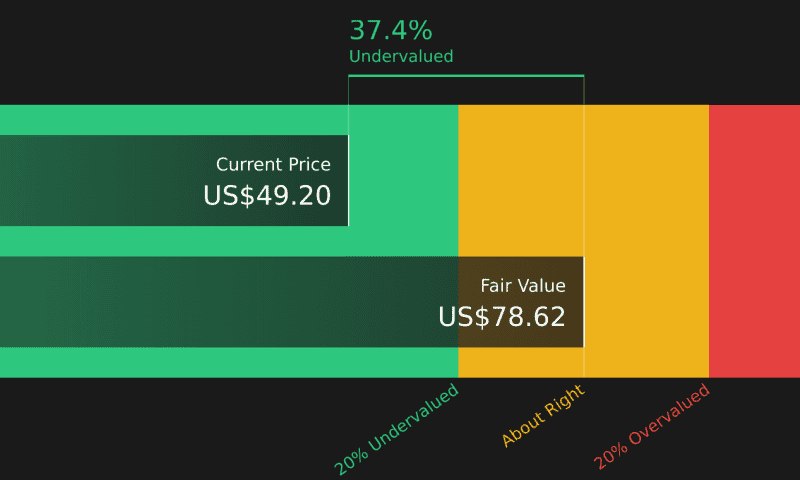

While the analyst narrative flags Hewlett Packard Enterprise as 64% overvalued at a fair value of about $29.92, the SWS DCF model points the other way. On that view, HPE at $49.20 trades about 38% below an estimated fair value of $79.23, which is a wide gap for investors to think through.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hewlett Packard Enterprise for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.