Get insights on thousands of stocks from the global community of over 7 million individual investors at Simply Wall St.

Antero Midstream (AM) stock has drawn investor attention after recent trading left the shares around $21.52, putting fresh focus on how the company’s midstream and water handling business supports its current valuation.

The current US$21.52 share price comes after a mixed stretch, with the stock easing slightly over the past quarter. At the same time, the year to date share price return of 19.96% and a 5 year total shareholder return of 190.73% point to momentum that has built over a longer horizon.

If you are comparing Antero Midstream with other income and infrastructure focused ideas, it can be useful to scan for 33 power grid technology and infrastructure stocks as a next step in your research.

With the stock near US$21.52 after strong multi year returns and solid reported revenue and net income figures, the key question now is whether Antero Midstream is still undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 8% Undervalued

The most followed narrative pegs Antero Midstream’s fair value at $23.29, a touch above the recent $21.52 share price and built on long term cash flow assumptions.

Long-term, exclusive contracts with Antero Resources, combined with over 20 years of high-quality, dedicated natural gas inventory, ensure stable minimum volume commitments, supporting strong earnings visibility and reducing risk for future net margins.

Want to see what sits behind that forecasted cash flow stream and fair value gap? The narrative leans heavily on steady volume growth, rising margins, and a richer future earnings multiple that together shape its long run valuation story.

Result: Fair Value of $23.29 (UNDERVALUED)

However, the story could change quickly if Antero Resources scaled back activity in Appalachia, or if tighter environmental rules raised costs and squeezed margins.

Wall Street’s queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab’s valuation page.

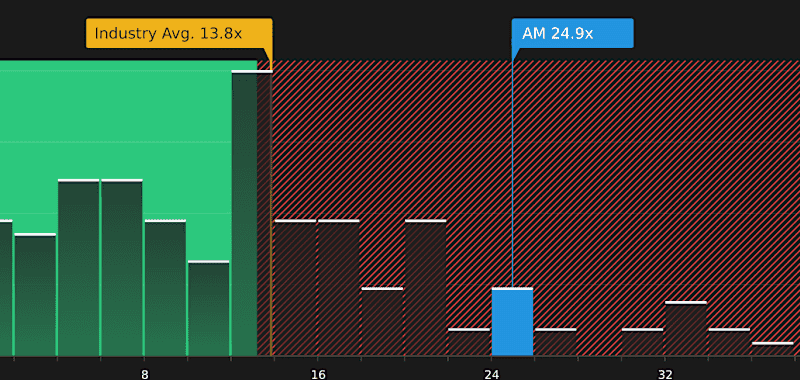

Another View: Earnings Multiple Sends A Different Signal

That 8% discount to the $23.29 fair value sits awkwardly beside the current P/E of 24.9x, which screens as expensive versus a fair ratio of 22.1x, a peer average of 18.7x, and an industry level of 13.8x. Is the stock priced for more growth risk than the DCF narrative suggests?